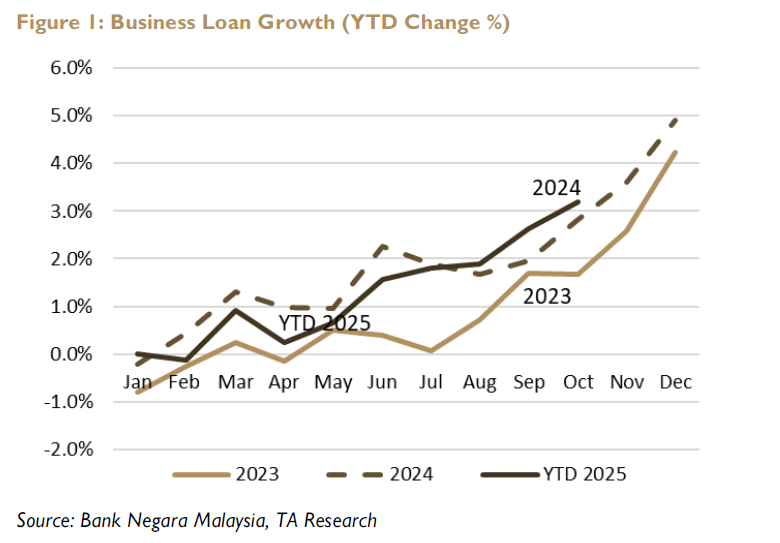

LOAN growth in 2025 began sluggishly but rebounded following U.S. tariff adjustments. By October, business lending had expanded 5.3% year-on-year (YoY), with year-to-date (YTD) growth outpacing 2024 levels of 2.8%.

Momentum was strongest among SME-focused and mid-market banks, while wholesale and large corporate banking delivered more uneven results.

Household loan demand remained resilient, though it moderated slightly to 5.4% YoY.

The sector continues to lean toward mortgages, unsecured lending, and credit cards, and banks are expected to pivot further into high-margin segments in 2026 to protect profitability.

Overall loan growth is projected at 5.7% in 2026, underpinned by 5.8% growth in consumer lending and 5.5% growth in business loans.

Average Net interest margin (NIM) contracted in the nine months of 2025 (9M 2025) to 1.98%, weighed down by Bank Negara Malaysia (BNM)’s policy rate cut and intensifying competition.

Looking ahead to 2026, effective liability management and the pursuit of low-cost deposit growth will be critical to margin preservation.

Larger banks are expected to continue expanding their current account and savings account (CASA) share, while smaller banks focus on targeted deposit initiatives to remain competitive.

“Our forecast anticipates a modest 3 bps YoY narrowing to an average of around 1.95% in NIM for 2026, assuming no further reductions in current Overnight Policy Rate (OPR) of 2.75%,” said TA Securities.

In 2026, non-NII is projected to grow by 9.6%, supported by cross-sell strategies, trading and investment gains, and structural initiatives that leverage client relationships, market volatility, and specialised segments.

Larger banks are expected to benefit from their scale and regional dominance in wealth management and capital markets, while smaller banks aim to stay competitive through partnerships, mergers and acquisitions, and digital investments.

Banks are expected to balance strategic investments with disciplined cost management, as operating expenses rise about 6.0% in 2026 on the back of inflation and continued technology spending.

Personnel costs are being contained through controlled hiring and redeployment into higher-value roles, while larger technology investments aim to strengthen long-term capabilities.

Overall, the sector’s Cost-to-Income Ratio (CIR) is forecast to remain broadly stable at 46.4%, as steady income growth cushions cost pressures and supports profitability.

Asset quality in the banking sector has remained resilient, with impaired loans trending lower, falling 3.8% YoY.

“We note of YoY improvements across both consumer (-0.6% YoY) and business (-7.9% YoY) portfolios, respectively. Loan loss charges stayed within guidance, though coverage ratios varied,” said TA.

Looking ahead to 2026, the outlook is broadly stable, supported by a resilient domestic economy, though banks are exercising greater caution in vulnerable segments.

Gross credit costs are expected to remain contained at 26–27 bps, while the average sector GIL ratio is forecast to hold steady at around 1.4%.

For 2026, TA’s stock-picking strategy centres on SME and business loan growth as a key driver of credit expansion, complemented by targeted high-yield lending to bolster margins and profitability.

TA sees significant upsides cross-selling opportunities across wealth management, client services, and capital markets, which diversify income streams and reduce reliance on traditional lending.

Larger, tech-forward banks are positioned to benefit from economies of scale and digital adoption, capturing efficiencies and sustaining competitive leadership in a rapidly evolving landscape.

Against this backdrop, TA maintains an Oerweight stance on the sector, with CIMB Group Holdings Berhad, Malayan Banking Berhad, and Alliance Bank Malaysia Berhad as their top recommendations. —Dec 31, 2025

Main image: Fiscal Investor