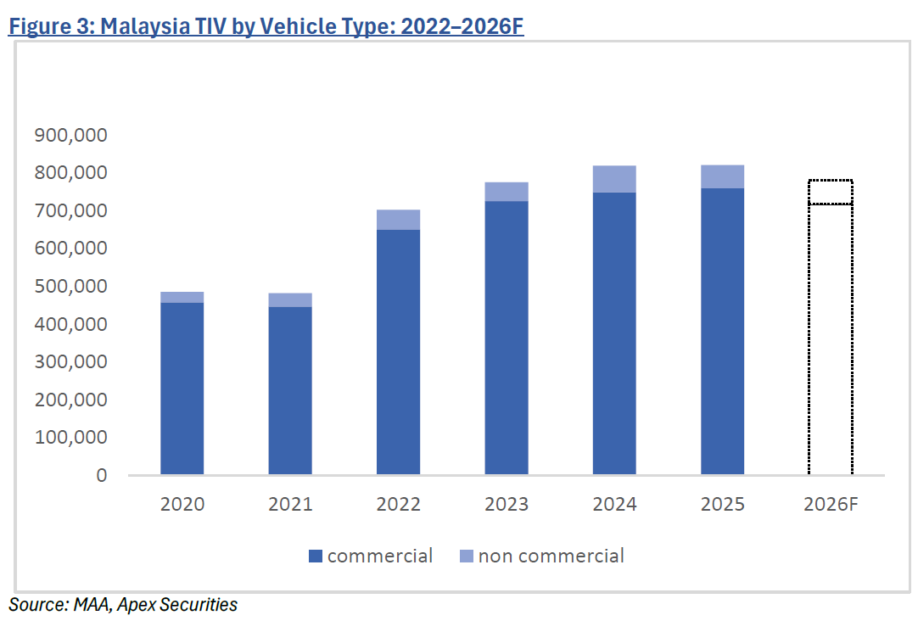

MALAYSIA’s Total Industry Volume (TIV) reached a new high of 820,752 units in 2025 (+0.5%) year-on-year (YoY), exceeding APEX Securities’ 770k forecast by 6.6%.

The outperformance was driven by a record December 2025, with MAA-reported registrations of 90,716 units (+11.0% YoY) as quarter four financial year 2025 (4QFY25) registrations of 241,416 units provided strong momentum to close the year.

“We view FY25 as a cyclical peak, supported by policy-driven purchase acceleration ahead of EV tax changes and resilient national OEM demand, rather than a sustainable step-up in underlying industry demand,” said Kenanga.

Kenanga introduced a lower 2026F TIV assumption of 780,000 units (-5.0% YoY), reflecting a persistent competitive environment within the non-national segment and the lack of near-term catalysts to meaningfully lift industry demand back toward prior peak levels.

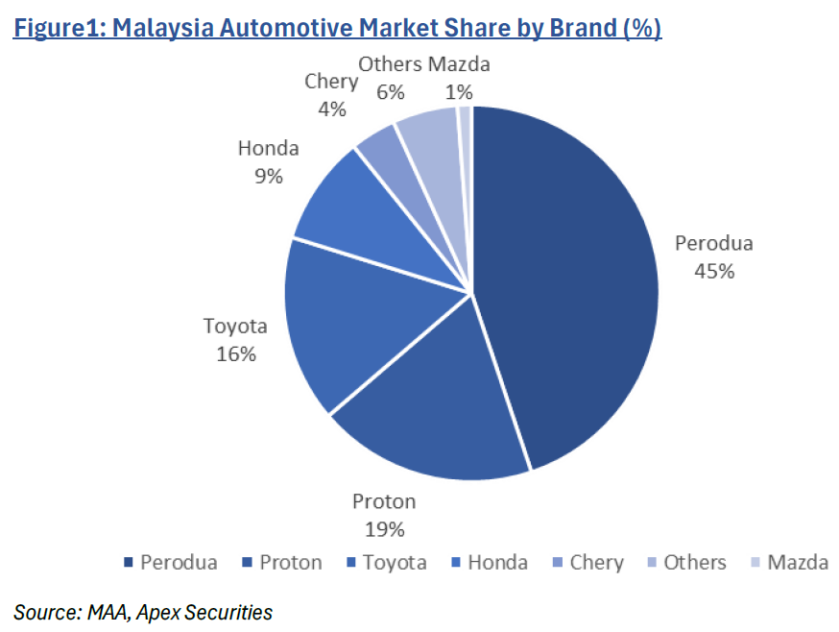

Perodua delivered its fourth consecutive record year with volumes of 360k units (+0.5% YoY) supported by sustained demand for core models (Bezza, Axia, Myvi).

Notably, Bezza exceeded 100k units for the second straight year, underscoring strong brand loyalty in the affordable segment. Proton also outperformed (+3.3% YoY), supported by new and facelifted models, with X50 volumes up 18.6% YoY, reflecting improving appeal of the SUV offering within the mass-market segment.

Honda volumes declined 11.3% YoY to 75,599 units due to heightened competition, while Toyota remained resilient (+1.5% YoY to 129,085 units) supported by its hybrid offerings.

Chinese marques continued to gain share, with BYD (+68% YoY to 14,407 units) and Chery (+61.0% YoY to 31,666 units) driven by competitive pricing and strong SUV demand.

Meanwhile, production lagged registrations, with 747,780 vehicles manufactured in 2025 (-5% YoY), underscoring the elevated reliance on CBU imports ahead of the EV incentive expiry.

What is slowing the EV adoption? Charging infrastructure remains a gating factor. According to the Energy Commission Malaysia (ST), Malaysia currently has fewer than 6,000 public EV charging points nationwide with DC fast chargers heavily concentrated in the Klang Valley and major highways.

This remains well below the government’s 10,000-charger target by end of 2025 under the Low Carbon Mobility Blueprint (LCMB) 2021–2030, largely due to slower-than-expected AC charger deployment.

As a result, EV adoption remains urban-centric, skewed toward second car households, fleet operators and early adopters rather than broad-based mass-market penetration.

While national OEMs are expected to remain relatively resilient, sustained competition within the non-national segment, pricing pressure, and limited near-term policy catalysts are likely to cap sector re-rating potential.

Downside risks remain skewed toward softer order flows and margin compression, particularly for foreign OEMs with higher CBU exposure. —Jan 28, 2025

Main image: WDA Automotive Marketing