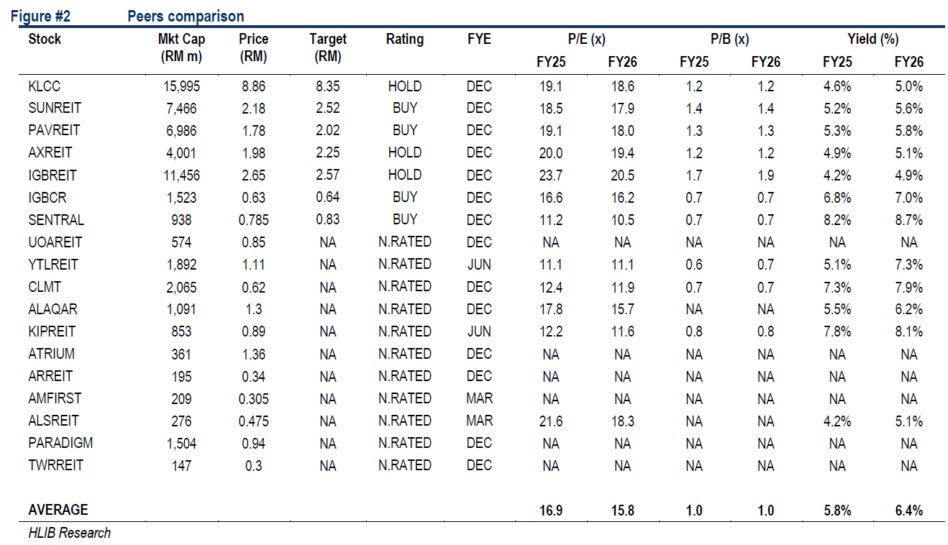

DURING the recent results season, five of the six REITs under Hong Leong Investment Bank’s coverage delivered earnings that were generally in line with both they and consensus expectations (SENTRAL, IGBCR, AXREIT, KLCC, Pavilion REIT).

Revenue for most REITs was flattish to slightly higher quarter-on-quarter (QoQ), reflecting limited seasonality in the office and industrial segments, while the retail segment saw no festive-driven uplift as both quarter two 2025 (2Q25) and 3Q25 lacked major festivals.

“Sunway REIT was the standout, posting 11.8% QoQ revenue growth, supported by a 109.1% surge in its hotel segment, marking its highest quarterly hotel revenue since listing driven by strong MICE demand,” said Hong Leong Investment Bank (HLIB).

Pavilion REIT also recorded a 6.8% QoQ increase, supported by the first full-quarter contribution from Banyan Tree Kuala Lumpur (BTKL) and Pavilion Hotel Kuala Lumpur (PHKL) following their injection on 20 June 2025.

Sunway REIT, Pavilion REIT, Axis REIT, and KIPREIT delivered double digit year-on-year (YoY) growth driven by recent acquisitions and firmer rental performance. Sunway REIT benefitted from the injections of Sunway 163 Mall in October 2024, Kluang Mall in December 2024, Sunway Oasis at Sunway Pyramid in November 2024, and Aeon Mall Seri Manjung in July 2025, which strengthened its retail portfolio, alongside the completion of Phase 2 of the refurbishment of Sunway Carnival Mall in May 2025.

Pavilion REIT continued to benefit from the two hotel injections highlighted earlier. Meanwhile, KIPREIT recorded growth supported by the acquisitions of KIPMall Desa Coalfields, KIP Kuantan, and Bintulu Industrial Land, which were completed between August and September 2025.

“Looking ahead, we expect sector earnings to be underpinned by company specific strategies such as asset injections, tenant remixing, and improving occupancies, while retail REITs in 4Q25 should also benefit from the seasonal uplift during the year end festive period and school holidays, which typically drive higher tenant sales and variable rents,” said HLIB.

From 4Q25 onwards, REITs with recently completed acquisitions should see stronger contributions, and IGBREIT’s earnings will be supported by the injection of Mid Valley Southkey completed in November 2025.

Office recovery story continued to strengthen across the sector, with most REITs reporting higher occupancies and sustained positive rental reversions.

Despite ongoing oversupply in Klang Valley, the broad-based occupancy uplift indicates that office recovery is firmly underway, supported by improving tenant demand and flattish to positive rental reversions.

HLIB maintains the OVERWEIGHT stance on the sector, underpinned by its:

(i) inherent defensive characteristics.

(ii) resilient income profile.

(iii) attractive valuations.

“In our view, Malaysia’s pivot toward high-tech and highvalue sectors is creating structural demand for office-based functions such as R&D, design, and regional operations,” said HLIB. —Dec 16, 2025

Main image: Shutterstock