IN the daily churn of Bursa Malaysia, hot thematic stocks often overshadow legacy companies undergoing genuine fundamental transformations.

This is where Mentiga Corp Bhd, a Pahang state government-linked company (GLC) represents a compelling case of value discovery.

Having quietly ended a four-year streak of losses to return to the black, the group has largely bypassed the radar of both institutional and retail investors.

Beyond its earnings recovery lies a deeply hidden asset base and a valuation discrepancy that warrants closer inspection.

From timber to prime plantation

Historically tied to the traditional timber trade, Mentiga has executed a decisive operational pivot.

By FY2024, the legacy timber segment was virtually phased out. In its place, the plantation division has emerged as the group’s core engine, contributing over 96% of total revenue.

This turnaround is backed by solid execution. Fresh fruit bunches (FFB) production surged by 51% year-on-year (yoy) in FY2024.

With the vast majority of its 2,973-hectare planted area in the five-to-15-year prime production phase and crude palm oil (CPO) prices sustaining around RM4,000/metric tonne (MT), Mentiga is well-positioned to generate resilient operating cash flows.

Diversification efforts into durian farming and mining further expand its long-term revenue base.

A masterstroke in corporate restructuring

Mentiga’s robust plantation footprint stems from a highly strategic “land-for-land” swap with the Pahang state government.

By exchanging its former Pekan plywood factory site for over 5,300 hectares of new concession land, its management effectively repaired a once-battered balance sheet and laid the foundation for today’s thriving agricultural business.

Despite this fundamental shift, the broader market remains oblivious to this sleeping giant. At a share price hovering near 53 sen currently, Mentiga’s market capitalisation sits at a micro-cap RM38 mil.

However, its balance sheet reveals a staggering net asset per share (NAPS) of RM3.12.

Trading at a price-to-book (P/B) ratio of just 0.15x, the market is essentially pricing RM1.00 of tangible book value at merely 15 sen.

Even within the generally undervalued plantation sector, an 85% discount to asset value is an exceptionally rare, bottom-tier valuation.

Trading at a steep discount

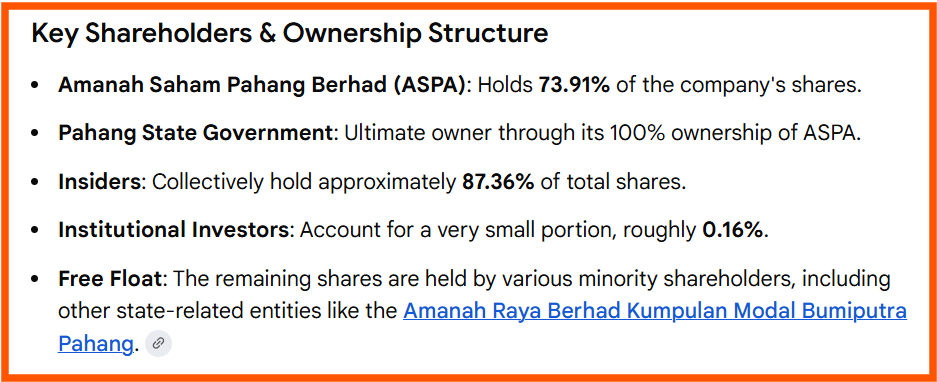

Why does this valuation gap persist? The primary factor is its shareholding structure. The Pahang state government’s investment arm Amanah Saham Pahang Bhd (ASPA) provided critical financial backing during the company’s darkest days, including a vital debt-to-equity swap.

While this ensures supreme corporate stability, the resulting concentrated shareholding has led to a severely low free float. This lack of trading liquidity naturally deters institutional funds and limits active analyst coverage.

Mentiga has decisively moved past its legacy struggles. While near-term dividend payouts may take a back seat as the company rebuilds cash reserves, the fundamental return to profitability is undeniable.

Until broader market liquidity improves or a clear value-unlocking catalyst materialises, Mentiga stands as Bursa Malaysia’s quiet, under-the-radar proxy for deeply undervalued agricultural land.

At the close of today’s (April 10) market trading, Mentiga was down 0.5 sen or 0.93% to 53.5 sen with 296,400 shares traded, thus valuing the company at RM38 mil. – April 10, 2026