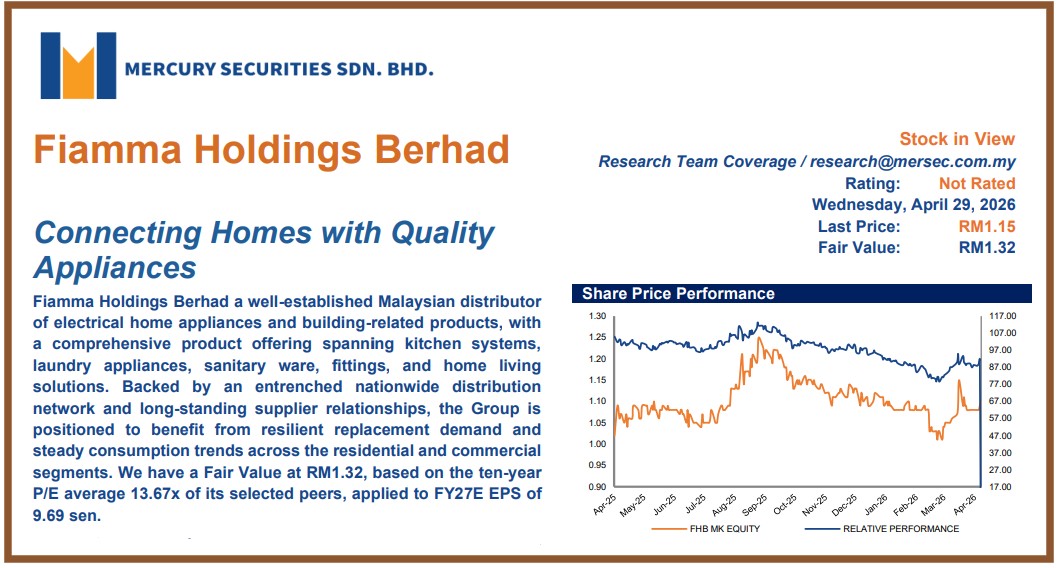

FIAMMA Holdings Bhd, a Main Market-listed home appliance maker/distributor, healthcare industry player and property developer, has been assigned a “fair value” rating of RM1.32 or a 18.5% premium to its yesterday’s (May 11) closing price of RM1.10 by Mercury Securities

According to Mercury Securities in its April 29 report entitled “Connecting Homes with Quality Appliances”, the fair value was derived based on a target price-to-earnings (P/E) multiple of 13.67 times – or a 10-year historical average P/E of selected peers – applied to Fiamma’s estimated FY2027 earnings per share (EPS) of 9.69 sen.

The research house described Fiamma as a well-established Malaysian distributor of electrical home appliances and building-related products with a product offering spanning kitchen systems, laundry appliances, sanitaryware, fittings and home living solutions.

Mercury Securities further noted that Fiamma is backed by an entrenched nationwide distribution network and long-standing supplier relationships which positions the group to benefit from replacement demand and steady consumption trends across the residential and commercial segments.

The report highlighted Fiamma’s Trading & Services segment as the group’s core earnings anchor.

The segment contributed 86.1% of FY2025 total revenue or approximately RM328.2 mil on the back of demand for essential household products, a diversified brand portfolio and broad market reach.

Household appliance market leader

Mercury Securities also highlighted Fiamma’s diversified business model which spans trading & services, property development and investment holding and property investment.

According to the report, this structure provides the group with a combination of stable, cyclical and recurring income streams.

On brand positioning, the research house noted that Fiamma’s in-house brands, including Elba, Faber and Rubine, continue to underpin its presence in Malaysia’s household appliance market.

Mercury Securities highlighted that Elba led the large cooking appliances segment with a 19% volume share in 2025, supported by product innovation and portfolio expansion.

Looking ahead, Mercury Securities expects Fiamma’s core earnings to register a two-year compound annual growth rate (CAGR) of 21% from FY2026E to FY2028E, supported by modest topline growth, steady demand across its core Trading & Services segment and continued expansion of its product offerings.

The research house also expects Fiamma’s gross profit margin to improve by approximately one percentage point from FY2026E onwards, supported by a better product mix.

It further projects the group’s pre-tax profit and net earnings margins to improve gradually from approximately 14% and 10% in FY2026E to approximately 19% and 15% in FY2028E respectively.

Mercury Securities noted that Malaysia’s home and living products industry is supported by steady household expenditure growth with mean monthly household consumption expenditure rising from RM4,080 in 2016 to RM5,566 in 2024 which represent a CAGR of approximately 3.9%.

It added that household formation, renovation activity and product replacement needs continue to support demand for home appliances and kitchen solutions.

At 4.40pm, Fiamma was up 1 sen or 0.91% to RM1.11 with 10,000 shares traded, thus valuing the company at RM589 mil. – May 12, 2026