ACCORDING to TA Securities, the PETRONAS Activity Outlook (PAO) 2026–2028 presents a balanced and pragmatic roadmap, as PETRONAS navigates economic volatility, geopolitical uncertainty and the long-term energy transition.

While the group continues to articulate its ambition to evolve into an integrated “energy superstore” and achieve net-zero emissions by 2050, the near-to-medium term strategy remains firmly anchored on sustaining core oil and gas operations to safeguard national energy security and cash flow resilience.

“Upstream activities, in our assessment, continue to prioritise domestic production sustainability, supported by intensified exploration, selective deepwater developments and new PSC awards, while downstream efforts focus on operational efficiency and gradual diversification into higher-value segments,” said TA.

At the same time, the PAO places greater emphasis on ecosystem readiness, with OGSE capability enhancement, productivity improvements and talent development identified as key enablers of execution.

“Overall, we view PAO 2026–2028 as evolutionary rather than disruptive, maintaining a stable upstream-led activity base while progressively embedding energy transition initiatives through collaboration, technology adoption and measured diversification,” said TA.

Against this backdrop, TA outlines below the key PAO 2026–2028 themes, which translate PETRONAS’ strategic intent into observable activity priorities, execution levers and implications for the broader OGSE ecosystem.

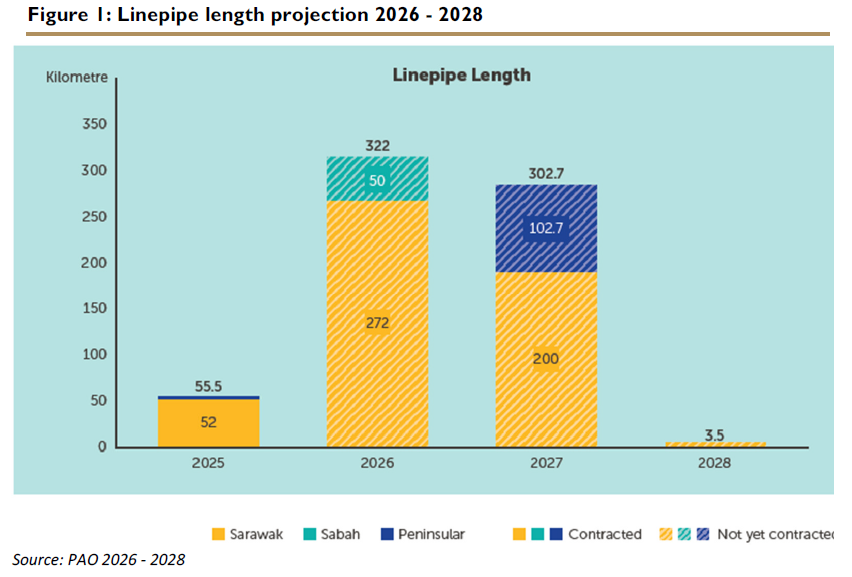

After missing the 2025 linepipe target of 346.6km, with only 55.5km delivered, PAO 2026–2028 indicates a sharp step-up in pipeline activity, with 322km scheduled for 2026, followed by 302.7km in 2027, before tapering to 3.5km in 2028.

The revised 2026–2027 volumes are materially higher than those outlined in PAO 2025–2027 (107.5km for 2026 and 14km for 2027), implying improved execution visibility and a stronger recovery in pipeline-related activity.

“We downgrade the sector from Neutral to Underweight, as PAO 2026–2028 does not point to a broad-based recovery but instead, reflects increasing divergence across segments,” said TA.

While turnaround works, pipeline activity and the improved outlook for fabrication of fixed structures provide selective pockets of support, persistent softness in OSV demand and the downward revisions in HUC man-hours are likely to weigh on sector-wide earnings momentum.

“In our view, the activity mix under the latest PAO suggests limited upside to aggregate earnings, with recovery concentrated in narrow scopes rather than signalling a cyclical upturn,” said TA.

The outlook highlights plant turnaround works in 2026 as the strongest near-term catalyst, positioning Steel Hawk as a key winner given its direct exposure to this front-loaded workload.

MHB also stands to benefit from the higher mix of EPCIC of WHP under the revised fabrication outlook, while PANTECH stands to gain from the step-up in pipeline volumes over 2026–2027, with sustained improvement in domestic O&G sales momentum serving as a potential re-rating catalyst. —Feb 13, 2025

Main image: Bidara Ventures