THE balance sheet strength of planters has generally improved in recent years, supported by prudent capital management, disciplined cash preservation amid relatively stable palm product prices, and the absence of major acreage expansion in both Malaysia and Indonesia due to ESG scrutiny and moratoriums on new land clearing.

“We expect planters’ balance sheets to strengthen further in the near term, supported by these same factors, as well as rising demand for renewable energy (particularly solar) and data centre developments across the country, which is driving interest in suitable land parcels for such projects,” said Hong Leong Investment Bank (HLIB).

A further strengthening in balance sheets, if it materialises, could lead to several potential outcomes:

(i) higher dividend payouts.

(ii) diversification into new business segments (such as renewable energy and property) by leveraging on existing landbank.

(iii) increased corporate exercises, including merger and acquisitions (M&A) and privatisation initiatives.

Of the 41 companies listed under KL Plantation Index, 26 were in net cash position as at their latest reported financial statements. This highlights the sector’s overall financial resilience and underscores the ability of many planters to enhance shareholder returns through higher dividend payouts, should they choose to do so.

The sector’s improving financial strength has also provided planters with greater financial flexibility to pursue new growth opportunities beyond their core plantation operations.

In recent years, several major players have diversified into non-plantation sectors, particularly renewable energy and industry property development, by leveraging their extensive landbanks.

These initiatives not only unlock latent land value but also create recurring, noncyclical income streams that help mitigate earnings volatility associated with commodity cycles.

“We note that larger planters such as IOI, KLK, and SDG have either indicated their intentions or commenced diversification projects as part of their long-term strategy to optimise asset utilisation, strengthen earnings resilience, and enhance shareholder value,” said HLIB.

The continued improvement in sector balance sheets could also pave the way for more corporate exercises, including M&A, strategic joint ventures, and privatisation initiatives.

In our view, better-capitalised players are now in a stronger position to pursue growth through consolidation and value-accretive transactions.

The stagnation in landbank expansion across Malaysia and Indonesia – due to stricter environmental regulations, government-imposed land moratoriums, and planters’ commitments to zero-deforestation and sustainable sourcing – will likely spur further consolidation within the sector.

Larger players may pursue acquisitions to enhance scale, efficiency and long term competitiveness, while smaller players could consider merger or asset divestments amid rising cost pressures and limited organic growth prospects.

Meanwhile, heightened ESG scrutiny among investors, has, to some extent, capped the investability of the plantation sector, potentially encouraging more privatisation activities.

Stricter sustainability requirements and rising ESG compliance costs have dampened investor interest in smaller, less liquid plantation stocks, leading to compressed valuations.

This may render such companies attractive privatisation candidates for major shareholders seeking to unlock long-term asset value.

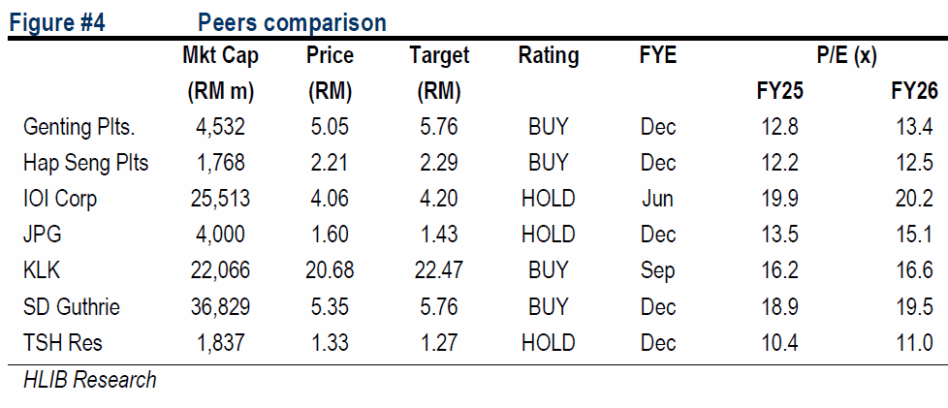

Some small-to-mid cap planters with solid asset backing but limited organic growth prospects may increasingly consider delisting. Within HLIB’s coverage, HSP and TSH exhibit these characteristics, given their strong balance sheets and relatively illiquid shares.

“Maintain Overweight on the sector, supported by a constructive outlook for crude palm oil prices over the near to medium term,” said HLIB.

HLIB prefers planters with greater exposure to Malaysian upstream operations, given their high leverage to CPO prices and minimal exposure to land confiscation risks. —Nov 19, 2025

Main image: Reuters