THE local property sector continues to show resilience despite signs of moderating momentum.

While loan applications eased in May following a strong April, analysts believe buying interest remains healthy, although higher living costs and tighter lending standards could temper demand in the months ahead.

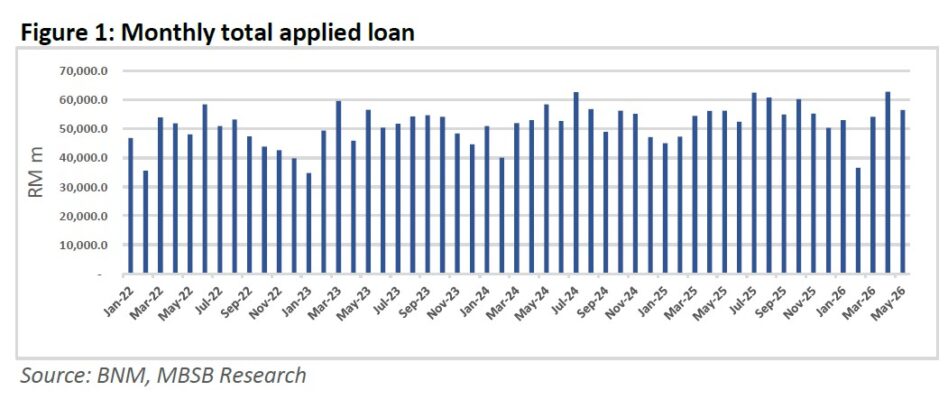

Total loan application for purchase of property was weaker at RM56.5 bil in May 2026 following strong growth of +15.9% month-on-month ()mom in April 2026.

The sequential decline was likely due to the public and school holidays in May 2026. On a year-on-year (yoy) basis, total loan application was flattish at RM56.5 bil (+0.3% yoy) in May 2026 after strong growth of +11.8% yoy in April 2026.

That brought the cumulative five months of the calendar year 2026 (5MCY26) total loan application marginally higher at RM263 bil (+1.4%yoy).

Overall, buying interest on property remains healthy, with inflationary pressures likely to have a modest impact on buying sentiment going forward.

Approved loan for purchase of property declined to RM24 bil (-10.7% mom) in May 2026, in line with the decline in loan application.

That brought cumulative approved loans to be muted at RM110.9 bil (-0.1%yoy) in 5MCY25. Overall, the lower approved loan was partially dragging by the lower approval ratio as banks are more stringent in loan approval.

KL Property Index gained +4.5% in the first half of 2926, outperforming KLCI marginal losses of -1%.

The top five gainers of property companies:

1/ MKH Berhad (+91.2%)

2/ Guocoland Malaysia Berhad (+86.3%)

3/ Bedi Berhad (+66.7%)

4/ IOI Properties Group Berhad (+49.2%)

5/ SP Setia Berhad (+32.9%)

Notably, the strong gain of MKH Berhad was on the back of Mandatory General Offer by Batu Kawan Berhad while strong gains of GuocoLand Malaysia was due to privatisation process initiated by its controlling shareholder, GLL (Malaysia) Pte Ltd.

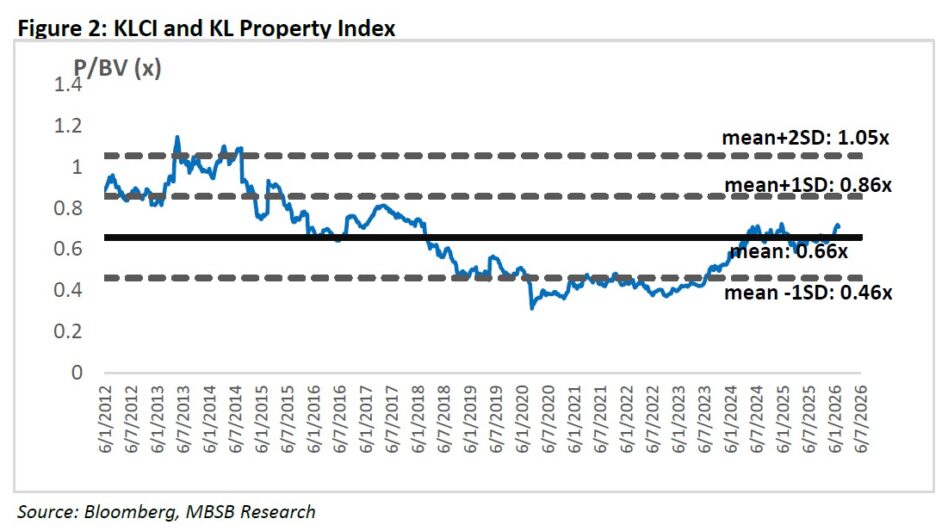

Meanwhile, performance of KL Property Index was largely unchanged month-to-date. KL Property Index is trading at price to book 0.68x which is slightly above its long-term mean of 0.66x.

“Hence, we believe the KL Property Index is fairly valued, with limited upside following the reversion of valuations to slightly above their historical average,” said MBSB Research.

MBSB maintains their Neutral stance as they expect a more measured outlook going forward. They see that the higher electricity costs, fluctuating fuel prices and rising logistics costs may gradually increase living costs.

While the impact has been manageable so far, these factors could lead to more cautious spending by households going forward.

“Despite our neutral outlook on the sector, we continue to see selective buying opportunities in stocks such as Matrix Concepts, IOI Properties Group and Mah Sing Group,” said MBSB.

The research house sees value in Matrix Concepts given its expected earnings recovery in 2027, attractive valuation and compelling dividend yield of 5.8% for 2027, with the recent share price weakness providing a buying opportunity.

Meanwhile, IOI Properties Group is well-positioned to unlock the value of its extensive landbank through active monetisation of non-core assets, while the proposed IOIPG REIT listing could improve balance sheet.

“On the other hand, we continue to favour Mah Sing, supported by its focus on affordable housing and healthy sales momentum,” said MBSB.—July 17, 2026

Main image: careerizma.com