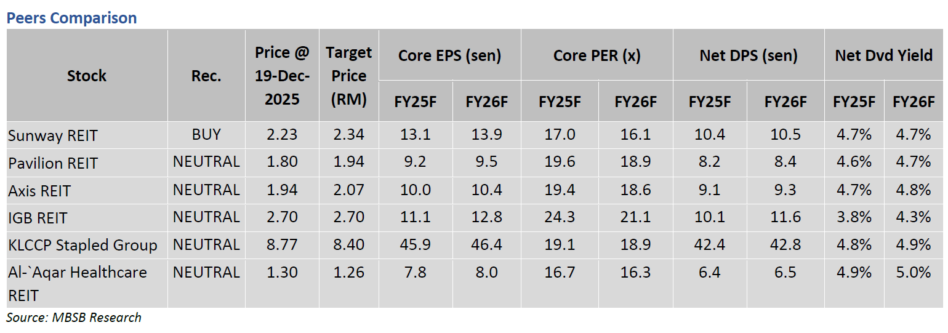

EARNINGS of REIT were largely in line in quarter three of calendar year 2025 (3QCY25), with four out of six REIT under MBSB Research’s coverage reported earnings that met expectations while two REIT reported earnings that beat its expectations.

Among REIT under their coverage, Sunway REIT recorded the highest earnings per unit growth of +29.6% year-on-year (yoy) in the nine months of calendar year 2025 (9MCY25) as earnings were spurred by the resilient earnings contribution from retail division while the strong earnings of hotel division aided earnings growth.

“Overall, all REIT under our coverage reported earnings growth in 9MCY25, in line with our expectation of better earnings prospect for REIT,” said MBSB.

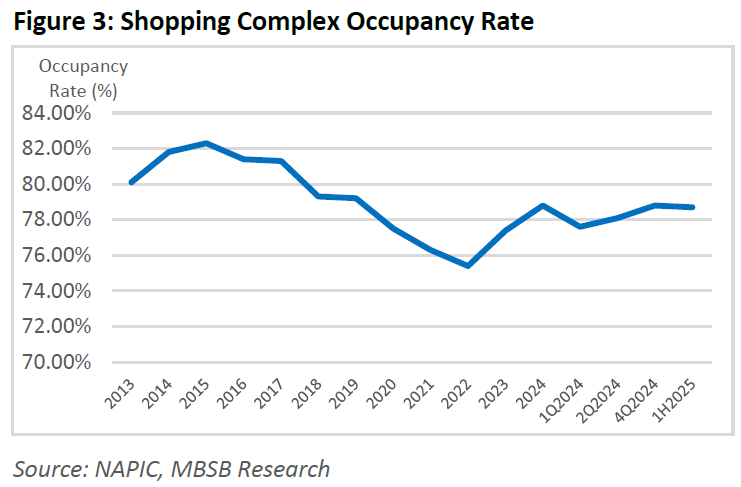

Retail segment in Malaysia is expected to remain bright going forward as occupancy rate of shopping malls remains decent.

According to data released by NAPIC, occupancy rate of shopping complex in Malaysia was stable at 78.7% in 2QCY25, largely unchanged from occupancy rate of 78.8% as of CY2024.

Meanwhile, shopper footfall is expected to be resilient in CY2026 due to robust retail backdrop and higher tourist arrival amid Visit Malaysia 2026.

The steady occupancy rate of shopping complex coupled with the anticipated higher shopper footfall should support growth of retail REIT in 2026.

Meanwhile, industrial transaction volume was higher at 4,148 units in the first half of 2025 (1H2025) against 3,822 units in 1H2024, indicating the strong interest on industrial properties in Malaysia.

“Hence, we see better prospect for industrial segment which should underpin positive rental reversion,” said MBSB.

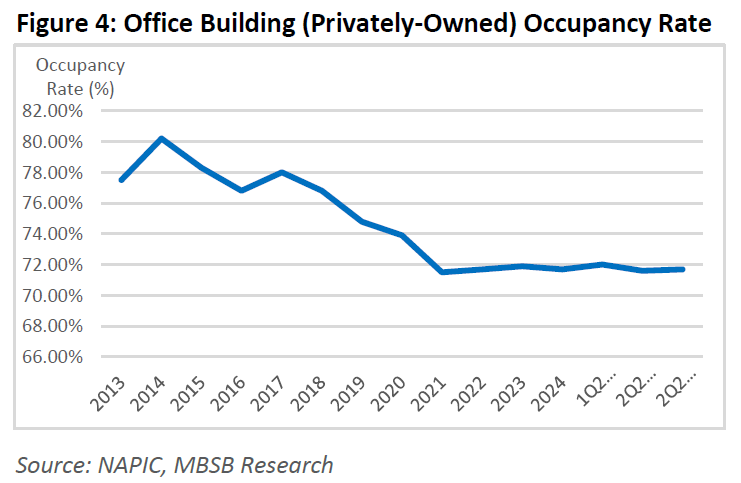

On the flip side, MBSB sees subdued prospect for the office segment as occupancy rate for privately-owned office buildings in Malaysia remains muted at 71.7% in 2QCY25.

Note that occupancy rate for office buildings in Malaysia declined from 74.8% in 2019 to 71.5% in 2021 due to increase in supply has subsequently stayed stagnant at 72% level.

The stagnant occupancy rate kept rental rate of office space muted. “Overall, we see that REIT with exposure to retail and industrial assets should see growth in CY2026 while office segment should see limited growth,” said MBSB.

“We continue to see stable earnings prospect for REIT in 2026, underpinning by positive rental reversion for REIT and Visit Malaysia 2026,” said MBSB.

Nevertheless, distribution yield of REIT under their coverage is compressed at average of 4.6% following the increases in share prices.

The narrowing yield spread between 10-year MGS yield and aggregate yield of KL REIT Index which fell below its long-term average is unattractive to investors.

“Hence, we maintain our NEUTRAL call on REIT,” said MBSB. —Dec 22, 2025

Main image: Plus 500