FOLLOWING SUNWAY’s takeover offer, IJM’s share price turned volatile last week amid a spate of negative news flow.

IJM confirmed that officers from the MACC and LHDN had visited its offices to obtain information.

It also disclosed that its Chairman, Tan Sri Dato’ Krishnan Tan, met with MACC officers, and that no fewer than 10 bank accounts were temporarily restricted to facilitate investigations.

Importantly, the group emphasised that these measures do not affect day-to-day operations.

Separately, the MACC confirmed its cooperation with the UK’s Serious Fraud Office in investigating an alleged RM2.5 bil money-laundering scheme involving IJM.

Despite these developments, SUNWAY reiterated that it will proceed with the takeover offer.

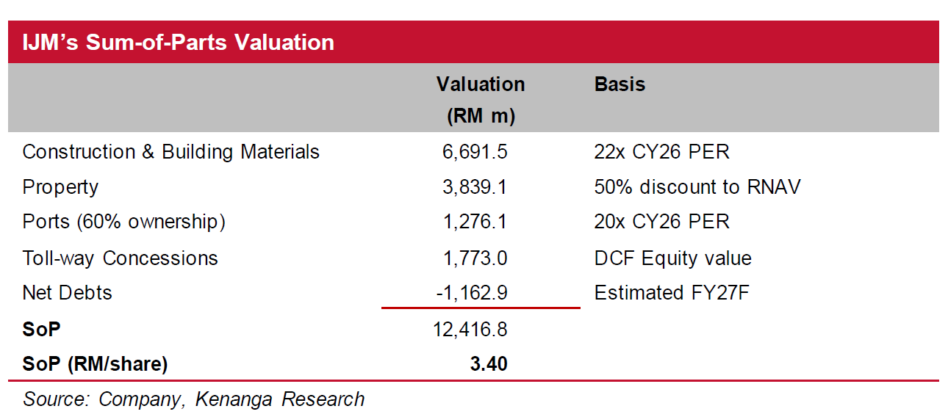

“The MACC news-driven sell-down has widened the arbitrage gap to 19%% vs. the RM3.15 offer price, while the current share price is now at a 29%% discount to our target price of RM3.40,” said Kenanga.

Based on their SUNWAY target price (TP) of RM4.73, the implied value of the offer for IJM of RM2.69 is nevertheless now slightly higher than IJM’s traded share price RM2.64, after IJM’s share price decline.

All said, given that their TP of RM3.40 is unchanged, implying more value to hold on IJM shares, Kenanga reiterates their REJECT recommendation on the takeover offer.

IJM targets RM6 bil–RM8 bil in order book replenishment for 2026, underpinned by multiple large-scale opportunities including three data centre jobs, two industrial projects, and the >RM1 bil Nusantara civil servant housing project.

Management expects to secure another hyperscaler data centre contract by end-financial year 2026. Other key prospects include the Penang LRT Mutiara Line (Package 2), Menara 118’s block, Penang Airport expansion, and road projects in Sarawak.

Kenanga likes IJM as it is poised to garner a slice of action in the Penang LRT Mutiara Line given its involvement in the previous LRT projects.

Also, its strong earnings visibility is underpinned by an outstanding construction order book of RM9.3 bil and new property sales of RM187 mil in quarter one of financial year 2026 (1QFY26).

Further note that its Kuantan Port is the largest port in the East Coast, capturing export and import activities growth, and the potential divestment of its toll road to lighten its balance sheet and recycle capital could act as a re-rating catalyst.

Kenanga maintains its Outperform rating. Risks to their call include sustained weak construction job flow, project cost overrun and liabilities arising from liquidated ascertained damages, and the rising cost of building materials. —Jan 26, 2026

Main image: Sinar Harian