IF YOU don’t know it by now, we at StashAway are big proponents of long term investing. One habit we encourage is investing a set amount of money on a regular basis (also known as dollar cost averaging, or DCA) to achieve your financial goals.

Having practised DCA over my working life, I must admit that it has helped me put aside capital and spread out my timing risk.

Not many of us who are white collar professionals who rely on monthly salaries have huge amounts to put aside at the start of our investing journey—only to check back after 10 to 20 years when we need the funds.

Similarly, as regular investors, the only time we’re able to time the bottom is in hindsight, when we say to ourselves, “I wish I’d invested in January 2009 in the depths of the Global Financial Crisis or in March 2020 when COVID-19 shutdowns were beginning”.

The best way to DCA is to select an investment and set up a direct debit or standing instruction so you don’t have to burden yourself with the administration and second guessing of investing.

Now, DCA only works if you invest in something that performs well after a period of time. Ultimately, your selling price still needs to be higher than your average buying price.

Four scenarios

I typically get the question, “Why DCA into a declining market?” to which I remind investors that accumulating investments when prices are low is advantageous in the long run and that part and parcel of long term investing.

DCA into a diversified portfolio, an index fund or blue-chip or large-cap stocks is the best way to go given that you don’t have to question the viability of the investment every time you invest your money.

However, this style of investing does not work on very speculative stocks or cryptocurrencies, as their prices could shoot up for a short period of time, only to crater and never recover again. What you expect of DCA is something that is fundamentally sound and will perform steadily over time.

To demonstrate this, here are four hypothetical friends who got together to invest individually in the S&P 500 index over the course of 21 years from January 2002 to December 2022. Each month they were supposed to invest $1,000 and only sell at the end of December 2022 (but there were slight variations because of their personalities and emotions).

Steady Steve is a straight-laced person who follows the rules. Without fail, Steve invested $1,000 monthly into the S&P 500 index fund over the time period. He set up a standing instruction, and only checked on his investments periodically without changing his investment plan.

He was concerned during certain stretches of bear markets, but he kept his nerve and never wavered.

Unlucky Luke thought he could somehow get ahead by trying to time the market. So he consulted his astrologer to ascertain if he should stay invested or if he should pull out all his money.

Because his astrologer had the star charts upside down, somehow he managed to instruct Luke to withdraw his investments just before the five best performing months within the 21 year stretch. Every time the astrologer would get it wrong, Luke would get into a fit, then promptly re-invest the money after the markets had a good month, hoping to catch the rally.

Anxious Ann has a habit of panicking and thought that she would try DCA to remove emotions from investing. She managed to stay invested for the most part, although she would panic after enduring certain bad months.

She would go through a particularly bad month, only to lose her nerve and withdraw all her money to spend one month on the sidelines.

She would regain her confidence and reinvest all of her money after a month away from the markets.Throughout the investment period, she did this five times, withdrawing her money after the top five worst performing months.

Finally, the fourth friend, Savvy Sally, who had some investing knowledge and a disciplined mindset, did something a little different. Instead of just investing $1,000 each month, she would invest $2,000 when markets were particularly bad.

She figured this predetermined response would be the best way of dealing with her anxiety when markets were in panic mode. Sally would in essence be performing value cost averaging, a variation on DCA, which dictates that the lower prices go the more one invests, thus accumulating more investments at lower prices in the process.

Value-cost averaging is a practise that takes both guts and discipline to carry out. Sally invested additional funds during the top five worst performing months of the process.

Final outcome

The four friends then reconvened after the long investment period to compare their approaches and investment gains. All four of them found it amusing that even though the goal was to simply invest $1,000 monthly for 21 years, they all had varying approaches and hence varying results.

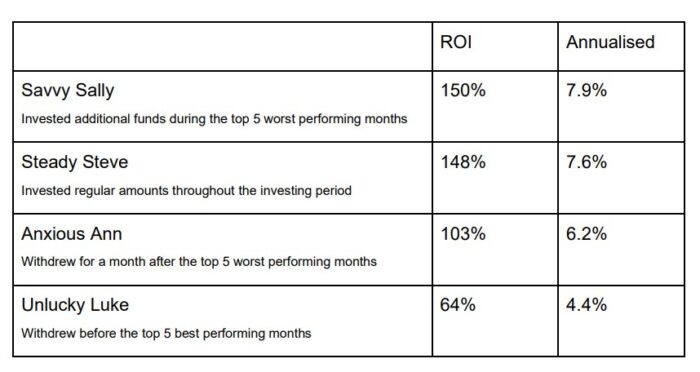

Steady Steve reported that he had made a total return on investment (ROI) of 148% which when annualised would work out to be 7.6%.

Unlucky Luke discreetly tucked away his star charts and said that he only made an ROI (return on investment) of 64% or 4.4% per annum but then remarked that he was just happy to not lose his capital.

Anxious Ann admitted that she withdrew after particularly bad months which yielded her an ROI of 103% or 6.2% per annum, and agreed with Luke that being in the black was a relief.

Lastly, Savvy Sally revealed that she had made an ROI of 150% or 7.9% per annum by investing more during market dips.

Everyone agreed that DCA for the most part, an easy process that took a huge mental burden off their minds. After all, they had each made investment gains despite their quirks. They also agreed they would have been better off had they just stuck to the rules or even had the courage to do what Sally did. – Feb 12, 2023

Wong Wai Ken, CFP, is the Country Manager StashAway Malaysia and a certified member of the Financial Planning Association of Malaysia (FPAM).

The views expressed are solely of the author and do not necessarily reflect those of Focus Malaysia.