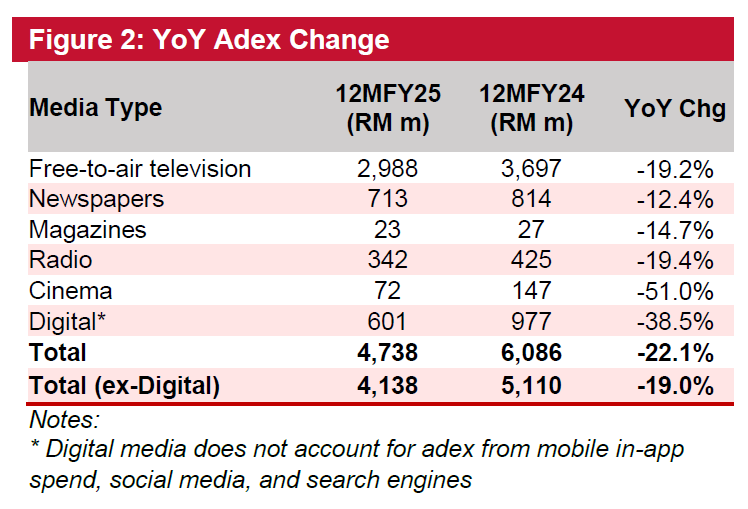

ADVERTISING expenses (adex) 2025 of RM4.74 bil (-22%) year-on-year (YoY) came in broadly in-line with Kenanga’s expectations, representing 97% of their full-year adex assumption of RM4.72 bil.

Weaker adex in 2025 was broad-based, led by the free-to-air TV segment (-19% YoY), where adex declined sharply at NTV7 (-44% YoY) and Awesome TV (-82% YoY).

The latter was likely impacted by the cessation of its broadcast on one of Malaysia’s major distribution platforms, ASTRO, since Aug 2024.

“In addition, we note that in Aug 2025, the network was embroiled in legal actions and public disputes related to alleged unpaid obligations to local content producers and artistes,” said Kenanga.

These recent developments may have weighed on advertiser sentiment toward the network.

Overall adex weakness in 2025 was further compounded by a sharp contraction in digital adex (-39% YoY), in line with weaker advertising spend on youtube.com (-39% YoY).

This likely reflects intensifying competition from other digital platforms, including social media, search engines and live commerce.

“In addition, we believe YouTube’s ad inventory has gradually shifted toward mobile and smart TV applications, to align with user consumption preferences,” said Kenanga.

For context, Nielsen Malaysia’s digidex tracking captures only display and video advertisements on desktop and mobile web pages.

youtube.com’s adex continued its rout for the 9th consecutive quarter, falling to RM95.5 mil in quarter four calendar year 2025 (4QCY25) (25% of its peak in 4QCY23).

CY25 newspaper adex slipped 12% YoY, with the bulk of the decline emanating from The Star (-42% YoY).

The weakness was broad-based across:

(i) MEDIAC (-40% YoY): primarily weighed by Sin Chew Daily (-44% YoY).

(ii) MEDIA: (-8% YoY): dragged by Harian Metro (-22% YoY) and, to a lesser extent, the New Straits Times (-8% YoY).

“For local incumbents such as MEDIA and ASTRO, we believe these trends offer a critical roadmap. While outright M&A is unlikely in the near term, strategic emphasis should be placed on the expansion of proprietary IP portfolios and strengthening brand franchises,” said Kenanga.

This can be achieved through the consistent production of commercially successful series and films that can be monetized across multiple windows—including linear TV, digital platforms, regional syndication, and international streaming partnerships.

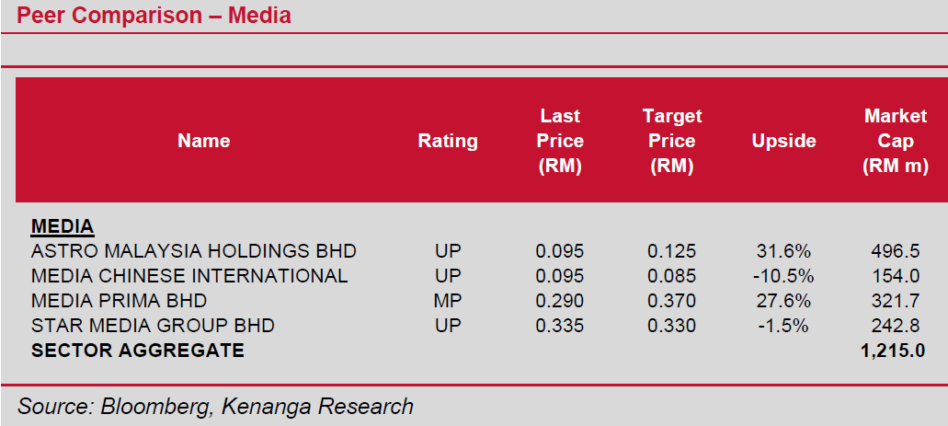

“We reiterate our UNDERWEIGHT call on the media sector, as earnings remain under sustained pressure from long-standing structural headwinds,” said Kenanga.

Competitive intensity continues to tilt in favour of digital-native platforms, which operate with more advanced technology stacks and lighter cost bases.

Conversely, traditional media players remain encumbered by sizeable fixed costs tied to legacy assets, for example, broadcast infrastructure, satellite capacity, printing operations and physical distribution fleets, which continue to dilute profits. —Jan 28, 2025

Main image: Sollok29