AVERAGE Brent crude oil forAug calendar year 2025 (CY25) slipped -14.7% year-on-year (yoy) and -3.3% month-on-month (mom) to an average of USD67.26 per barrel (pb).

The decline was due to increased global supply by non-OPEC+ countries, OPEC+ unwinding voluntary cuts, slow demand growth from economic slowdown, shift towards clean energy and lacklustre consumption in US and China, and higher oil inventory builds.

This is offset by the ongoing geopolitical tensions, with the recent Israel-Qatar bombing which risk sparking unrest in the Arab Peninsular.

Conversely, Henry Hub natural gas continues to gain in Aug CY25, by +38.5% yoy but declined -12.6% mom to an average of USD2.89p Million British Thermal Units (MMBtu).

“The upward surge was due to increased demand for power generation, following the summer season, rising LNG exports that outpaced production, and storage deficits in certain producing countries,” said MBSB Research.

“The upward surge was due to increased demand for power generation, following the summer season, rising LNG exports that outpaced production, and storage deficits in certain producing countries,” said MBSB Research.

However, the lower monthly comparison was attributed to higher global inventory levels that provided a buffer against the price spikes, higher production volume, and uncertainty in weather forecast amid the season transition.

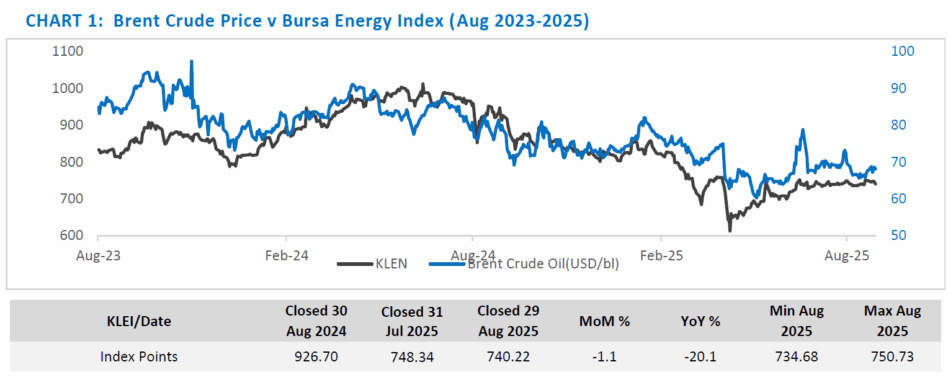

The KL Energy Index (KLEN) index’s Aug CY25 close was lower by -20.1% yoy and -1.1% mom. KLEN moved lower due to a confluence of global and domestic headwinds.

The sector is pressured by a persistent oversupply of crude oil, which is expected to reduce overall upstream capital expenditure.

Most major components reported a significant net loss for the second quarter of 2025 due to weak market conditions, a drop in plant utilization, and one-off charges.

Similarly, other OGSE companies were impacted by project setbacks and a challenging services market.

The market outlook for the Malaysian energy sector was generally “neutral,” reflecting a cautious sentiment and the expectation that a recovery would be gradual.

Given the expectation of weakening crude oil price in the second half of calendar year 2025 (2HCY25) onwards, we maintain a neutral call for the sector.

We see lesser upside in the sector, due to the expectation of a surplus in crude oil, which will subsequently cause crude oil to be traded in lower prices, impacting operations in the upstream and downstream that are closely tied to said prices.

However, we believe the midstream players will remain resilient, underpinned by the expected increase in demand for crude oil storage in the near to mid-term. —Sept 24, 2025

Main image: Comet