DESPITE late year de-risking, the sector’s underlying contract awards momentum remained healthy.

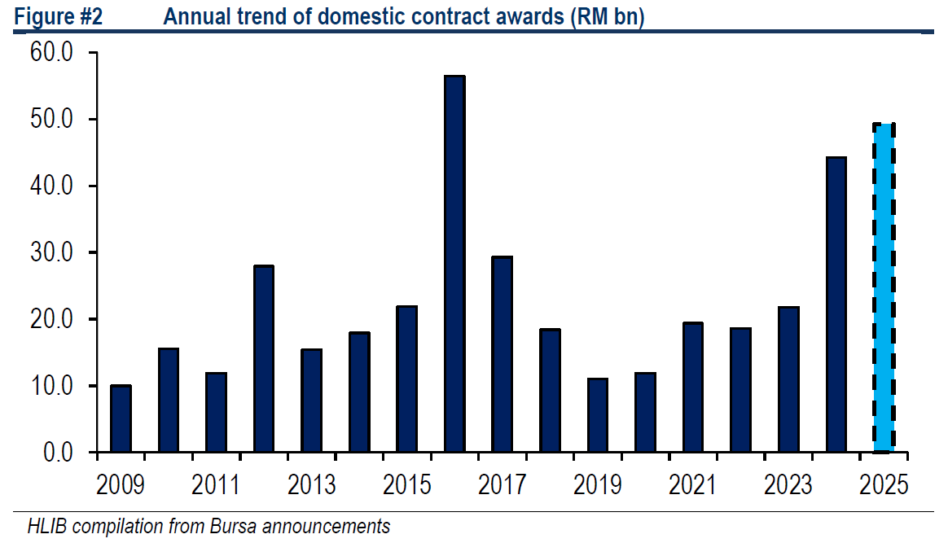

Hong Leong Investment Bank (HLIB)’s compilation puts the 2025 tally at RM49.2 bil of contract awards in 2025 increasing by 11.3% year-on-year (YoY), keeping the sector on an orderbook expansion path.

“While the 2025 tally deceptively falls short of the previous cycle high of RM56.4 bil in 2016, we think this understates the strength of the current cycle as the cumulative 2024-2025 contract value of RM93.4 bil is 9% higher than the 2016-2017 sum – thus, we anticipate a more sustained growth in the sector’s bottom-line performance,” said HLIB.

2025 contract flows were anchored by sizeable infrastructure conversion, led by Penang LRT Segment 1 (RM8.3 bil) and the LRT3 scope reinstatement VO (RM2.47 bil), and reinforced by other public sector mega jobs such as the Shah Alam Stadium redevelopment (KSSC) at RM2.94 bil.

Private sector momentum increasingly leaned on hyperscale data centres (DC) as DC derived contracts grew by 38% YoY, by HLIB’s estimates.

Nevertheless, due to staged rollouts some of the DC package awards were pushed into 2026. In 2026, HLIB expects headline job flows to run at a similar pace to 2024-2025, which remains adequate to expand sector orderbook.

The key anchor remains hyperscale DCs where 2026 could see larger campuses starting to take shape.

“The phased buildout should sustain award opportunities and a steadier annual replenishment profile. We gather that tendering pace has remained frenetic,” said HLIB.

Alongside DCs, HLIB sees the water segment as another orderbook driver in 2026, with multiple large schemes at different stages of rollout.

Notable multi-billion ringgit projects include the Northern Perak Water Supply Scheme, Ulu Padas Scheme, Rasau Stage 2 and Langat 2 Phase 2, among others.

Additionally, Penang LRT project continues to generate more job flows via subcontracts, Segment 2 and systems works, with the latter two potentially amounting to ~RM8 bil.

Separately, 2026 should see a continued build-up of the Johor-SG SEZ, supported by Budget-2026’s RM3.4 bil infrastructure development fund and HLIB expect further progress on the proposed Johor Bahru E-ART system.

“Finally, we do not expect MRT3 to be a material award driver in 2026 as land acquisition likely occupies most of the year; meaningful tender reactivation and awards are more likely to be pushed beyond 2026,” said HLIB.

Since the rollout of JPJ’s overloading enforcement crackdown (Ops Perang Lebih Muatan), HLIB channel checks suggests construction materials like cement and RMC saw higher average selling prices by ~20% and ~30% in Nov-25, largely reflecting pass-through of higher logistics costs.

Overnight stringent overloading enforcement has led to shortage of trucking capacity particularly specialised fleets, resulting in lower delivered volumes.

HLIB expects gradually normalising conditions in 2026 as the operation ends (31-Dec-25) while the supply chain also adapts through incremental capacity expansion.

“We retain our OVERWEIGHT sector call anticipating healthy contract flows in 2026 anchored by infrastructure projects and sustained DC rollouts,” said HLIB.

In our view, contractors can broadly still add to their orderbooks from the DC segment as well as infra projects. —Jan 7, 2025

Main image: Kallanish Commodities