KENANGA has retained its Neutral outlook on the telecommunications sector, citing persistent uncertainty surrounding Digital Nasional Bhd’s (DNB) transition to ownership by the mobile network operators.

The unresolved process continues to cloud visibility over the sector’s earnings outlook, capital expenditure plans and future dividend payments.

Nevertheless, the research house believes DNB’s privatisation may be nearing completion. This follows the latest capital injection, which has increased cumulative shareholder advances from each participating mobile network operator to RM552 million.

According to Kenanga, dividend prospects have also improved, providing some support for the sector.

TIMECOM is expected to benefit from balance sheet optimisation, while MAXIS and TM are backed by healthy free cash flow generation and relatively modest capital expenditure requirements.

With its 5G network now exceeding 80% Coverage of Populated Areas (CoPA), U Mobile is shifting its attention towards generating wholesale revenue. Its recent Mobile Virtual Network Operator (MVNO) agreements with VIBE Mobile, Eastel and TM reflect this strategy.

Kenanga noted that securing additional MVNO partnerships could further increase network utilisation, spread fixed infrastructure costs across a larger customer base and improve returns on its significant 5G investment.

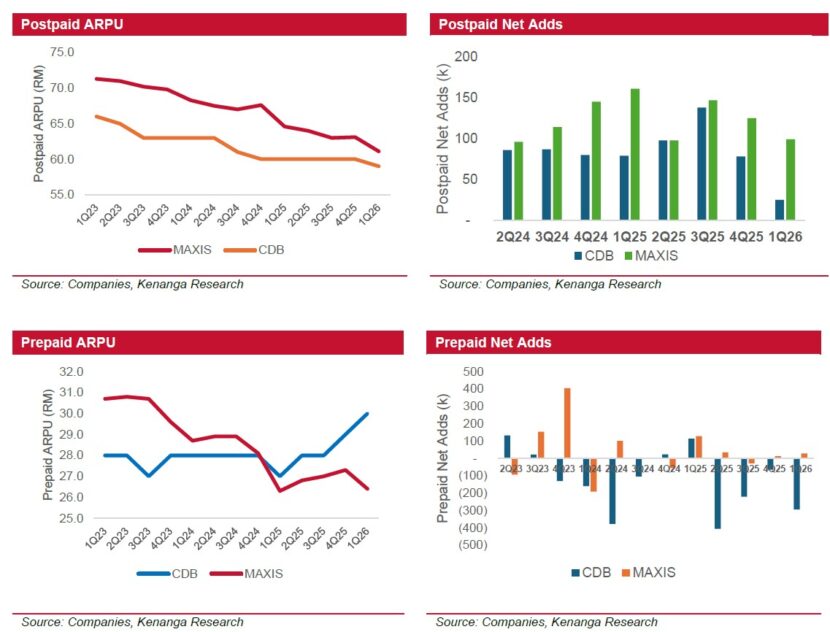

Meanwhile, the ongoing shift from prepaid to postpaid services remains a positive industry trend, supported by successful customer upselling, bundled service offerings and improving consumer purchasing power.

In the prepaid space, new MVNO entrants and U Mobile’s refreshed ULTRA5G plans signal rising competitive intensity. However, we expect competition to remain concentrated at the lower end of the market and centred on data allowances.

In the fixed-line segment, competition remains largely benign. Incumbents are holding headline pricing, while relying on localised guerrilla tactics to defend market share.

Meanwhile, 5G FWA is unlikely to pose a material long-term threat to fiber – given structural limitations in uptime reliability and speed consistency, particularly in dense urban environments.

“As 5G traffic volumes increase, we also expect mobile network operators to gradually moderate their FWA push to avert congestion risks,” said Kenanga.

The research house looks forward to further disclosures on Phase 1 of TM-Nxera’s 64MW hyperscale DC and a potential final investment decision on Phase 2 (136MW).

TIMECOM also remains steadfast in its DC ambitions, with AIMS progressing on its 200MW AI-focused DC JENDELA Phase 2 is finally underway, with Batch 1 contract awards anticipated as early as quarter three of 2026.—July 14, 2026

Main image: optiproerp.com