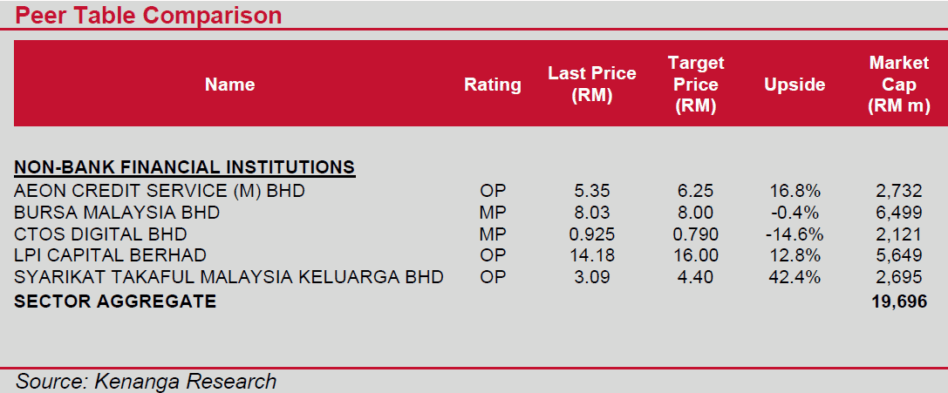

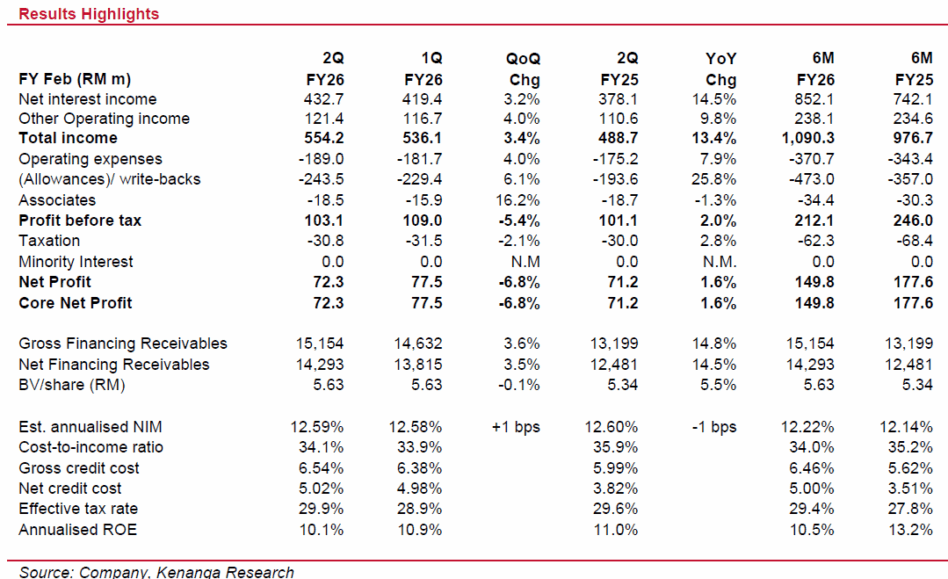

AEONCR’s first half of 2026 (1HFY26) net earnings of RM149.8 mil made up only 42% of Kenanga Research’s full-year forecast and 41% of consensus full-year estimate.

Year-on-year (YoY), 1HFY26 total income slid by 16%, no thanks to higher net credit costs of an annualised 5% (+149 bps), arising from more general provisions following greater delinquencies seen within the group.

Still, net interest income and gross financing receivables had grown concurrently by 15%. This supported the drop in cost-to-income ratio to 34% (-1.2 ppts) where the increase in operating expenses (+7%) remained led by personnel cost.

Meanwhile, Aeon Bank’s associate loss of RM34.4 mil during the period seems to be at the higher-end of the group’s annual guided loss of RM60 mil, which Kenanga believes could be attributed to higher marketing spend led by recent financing product roll-outs.

Quarter two financial year 2026 (2QFY26) net profit declined by 7%, mainly due to higher provisions. AEONCR’s mix of B40:M40 customers at 65:35 may likely pose some challenge to the group beyond 1HFY26, weighed down by lower economic prospects and inflation spurred by developments in trade tariffs.

Though the group is growing its loans well above its 10% target, we opine it may slow down on this effort to minimise its overall risk exposure and protect credit quality. Higher provisions led to return on equity (ROE) of 10.5%, falling behind the full-year target of 12.0%.

Meanwhile, Aeon Bank’s may see narrowing losses assuming its revenue generating products pick up, with new Islamic working capital financing products slated to be launched by Nov 2025. Investors may also be watchful of further potential rises in credit cost ahead of worsening macro conditions. Kenanga maintains outperform for AEONCR. —Sept 30, 2025

Main image: AEON Credit