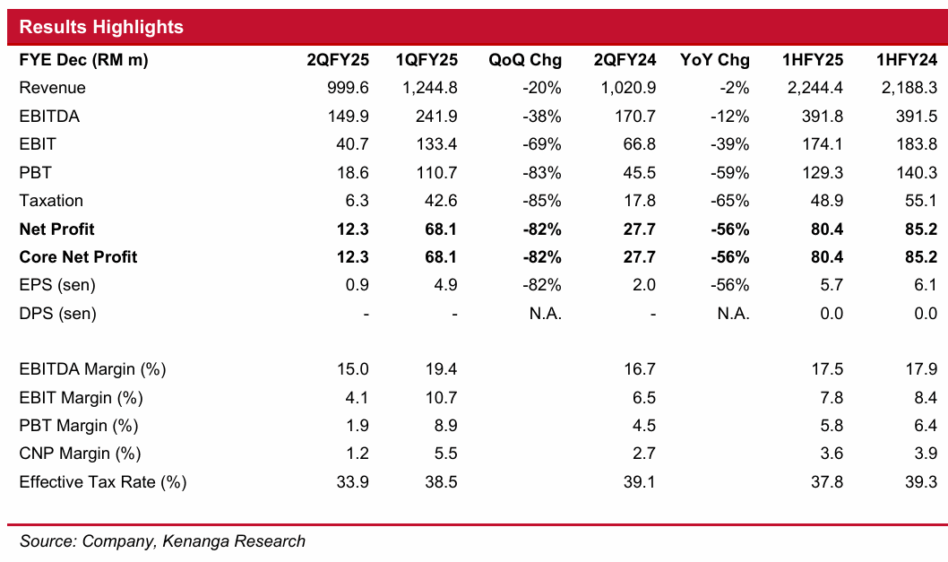

AEON’s first half of financial year (1HFY25) core net profit of RM80.4 mil met expectations at 54% and 48% of Kenanga Research’s full-year forecast and the full-year consensus estimate, respectively.

As expected, no dividend was declared during the quarter. Year-on-year (YoY), its 1HFY25 revenue rose marginally by 3% lifted by stronger PMS performance (+7%) on improved occupancy and effective rental renewals, which boosted segment profit by 18%, with margins also expanding by 3.8 points.

However, this was partially offset by its retail division, where earnings before interest and tax fell 52% weighed down by higher operating costs, despite a 2% revenue uptick. As a result, its 1HFY25 core net profit declined 6%.

AEON anticipates a gradual recovery in the retail sector in 2HFY25, underpinned by stabilising consumer sentiment and continued government support measures, while acknowledging that near-term margins could be pressured by expanded SST and electricity tariff hikes effective July 2025.

We concur with management on the margin outlook, noting also that 2H is seasonally softer and footfall is likely to be lower in quarter three (3Q) amid ongoing renovation works at several AEON malls and stores.

That said, resilient PMS contributions should continue to anchor profitability, including the upcoming AEON Mall KL Midtown slated to open in 2HFY26.

Additionally, we expect AEON to capture potential spillover gains from the RM100 one-off SARA cash aid, as the extra cash allows consumers to reallocate budgets towards discretionary purchases, providing a temporary boost for mass-market retailers.

We like AEON due to its ongoing mall refurbishments, which have led to sustained occupancy rates and favourable rental renewals for its property management services division.

Also, it has its strategic expansion of private-label offerings to enhance retail margins, and its digital transformation, particularly, the introduction of self-checkout for customers, that will result in cost savings.

While we are concerned over the near-term headwinds in the retail environment, we upgrade the stock to OUTPERFORM (from MARKET PERFORM), as we see potential value emerging with valuations.

Risks to our call include increased competition from both existing and emerging players, prolonged high inflation that may erode consumer spending power, and the ongoing shift towards online shopping, moving away from traditional in person shopping. —Aug 26, 2025

Main image: Bloomberg