GLOBAL OIL and gas markets are once again on edge as escalating tensions in the Middle East threaten to disrupt supply chains and drive up energy costs worldwide.

While RHB expects oil and gas prices to moderate over time, supply restoration is unlikely to be immediate, given restart lags and logistical constraints.

As such, oil prices are likely to stay elevated in the near term, supporting sector earnings.

“We see scope for near-term outperformance, particularly among midstream and selected upstream beneficiaries,” said RHB.

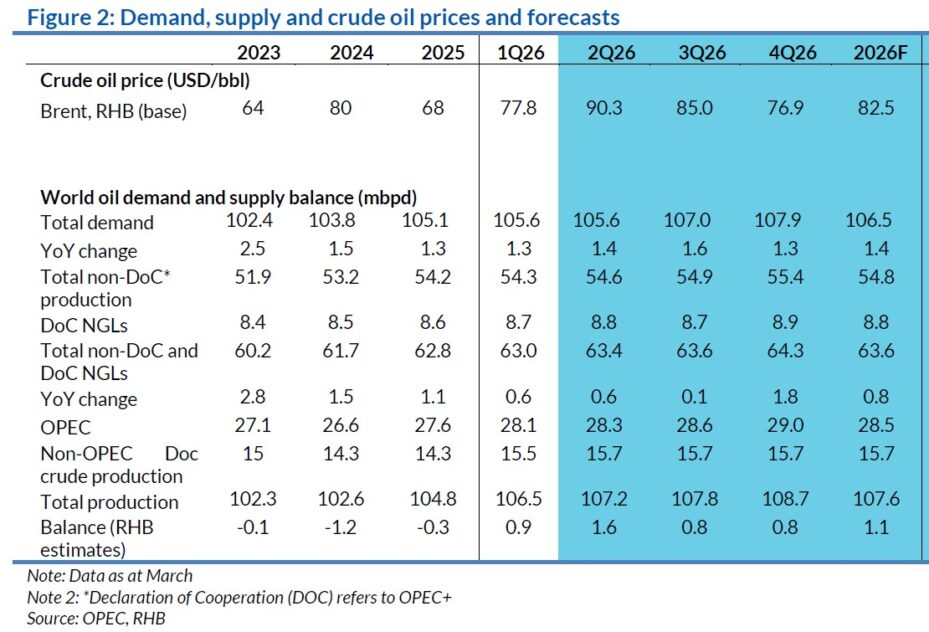

They raise their 2026 average Brent crude oil forecast to USD82.50/bbl from USD62/bbl and introduce a 2027 forecast of USD72/bbl.

As supply chains stabilise, RHB expects prices to settle around the mid-USD80/bbl level before trending lower towards our medium-term assumptions.

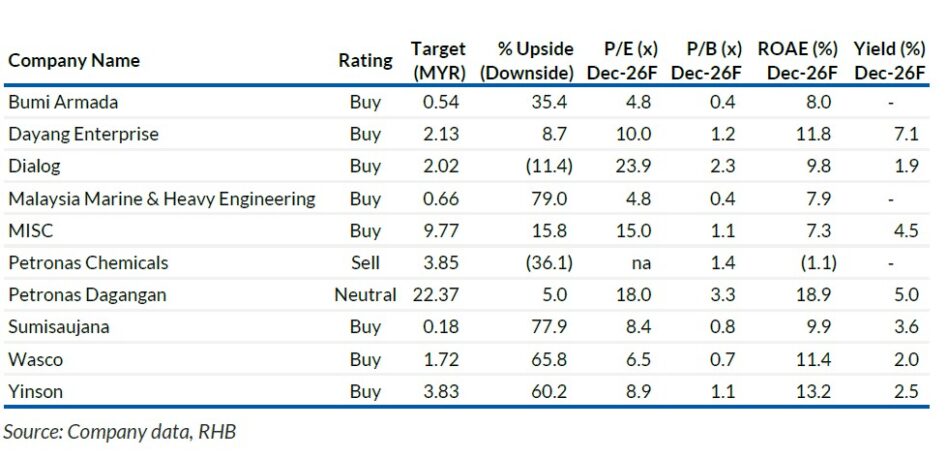

DLG offers partial upside to higher oil prices via its upstream exposure, while its core tank terminal and midstream businesses continue to provide stable and recurring earnings.

Meanwhile, MISC is well positioned to benefit from elevated tanker rates, as geopolitical tensions and supply disruptions tighten vessel availability and increase freight demand.

Petronas Chemicals (PCHEM) may emerge as a key beneficiary in a more protracted conflict scenario, where sustained supply disruptions and elevated oil prices could keep petrochemical markets tight – supporting higher product prices and improving spreads.

“However, we believe the extent and sustainability of this upside remains uncertain, as it is highly dependent on the duration of disruptions and underlying demand conditions,” said RHB.

Key risks to RHB call is the weaker-than-expected oil prices and global demand, particularly from China.

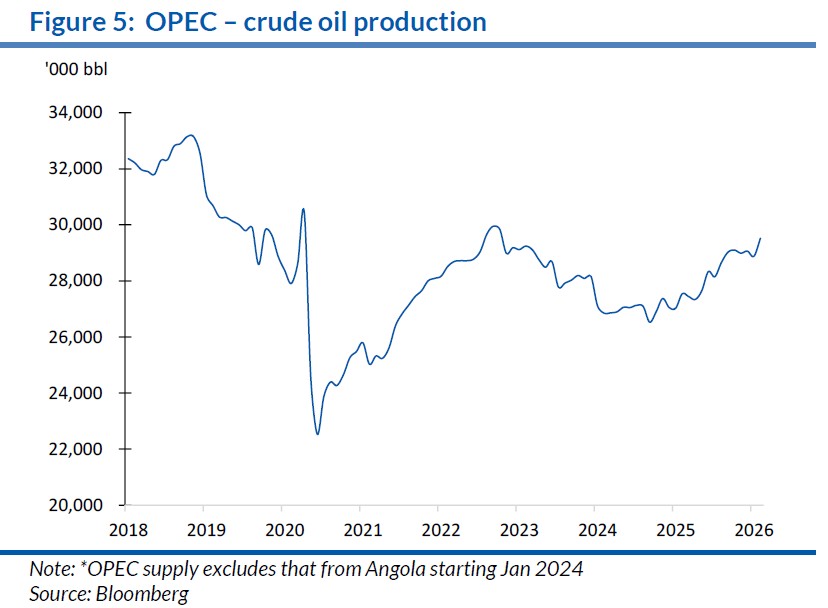

OPEC still sees healthy demand growth, albeit with emerging downside risks. Global oil demand growth is expected to remain resilient at 1.4mbpd year-on-year in 2026, unchanged from the previous assessment, driven largely by non-Organisation for Economic Co-operation and Development (OECD) regions, particularly Other Asia, India, and China, while OECD demand growth remains modest at 0.15mbpd YoY.

Demand is supported by strong air travel, healthy road mobility, and sustained industrial, construction, and agricultural activities in emerging markets.

This is alongside continued petrochemical capacity additions supporting feedstock demand such as NGLs/LPG and naphtha.

From a product perspective, gasoline and jet fuel are expected to contribute meaningfully to growth, with diesel also showing steady expansion, partially offset by weaker residual fuel demand.

“That said, we note that the recent surge in oil prices could pose some downside risks to demand if sustained, particularly through potential demand destruction effects,” said RHB.

Looking ahead, demand growth is projected to remain broadly stable at 1.3mbpd YoY in 2027, with non-OECD economies continuing to drive the bulk of incremental demand. —Apr 14, 2026

Main image: dow.com