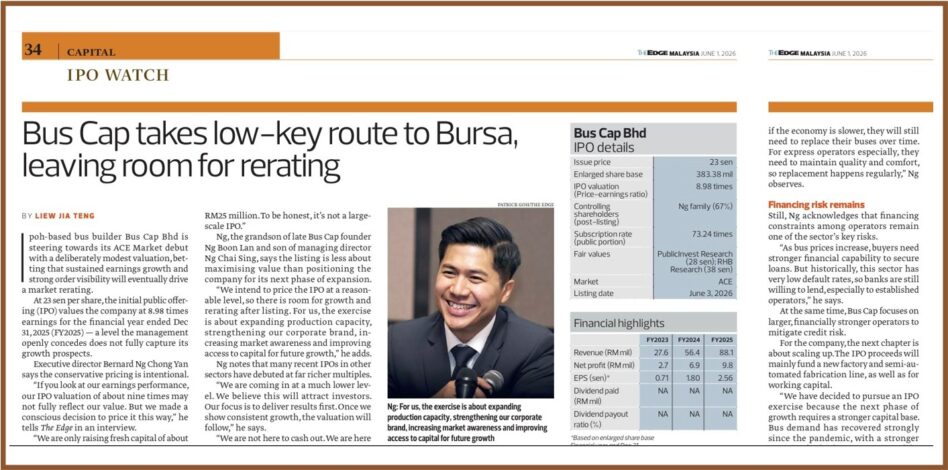

BUS Cap Bhd is not coming to Bursa Malaysia’s ACE Market tomorrow (June 3) with a loud valuation story. In fact, its IPO (initial public offering) appears to be built around the opposite idea – price it reasonably, leave room for the market and let earnings do the talking after listing.

That was the main message from a recent The Edge Malaysia interview with Bus Cap executive director Bernard Ng Chong Yan who described the group’s IPO valuation as conservative despite its strong earnings growth.

At an IPO price of 23 sen/share, Bus Cap is valued at about 8.98 times its FY2025 earnings with an estimated market capitalisation of RM88.18 mil upon listing.

For a company that more than tripled revenue from RM27.6 mil in FY2023 to RM88.1 mil in FY2025, the valuation does not look stretched.

Its net profit also spiked to RM6.9 mil in FY2024 and RM9.8 mil in FY2025 from RM2.7 mil in FY2023. This is not a company coming to market before proving its earnings base.

It is coming to market after showing that the recovery in bus demand has already translated into real profits.

A modest IPO with clear intention

The interesting part of Bus Cap’s IPO is that its management appears to have deliberately avoided aggressive pricing.

According to The Edge Malaysia, the IPO valuation of about nine times “may not fully reflect” the group’s value but the pricing was a conscious decision. The aim is to give the market room for growth and potential rerating after listing.

That is a very different message from many IPOs that try to extract maximum valuation upfront.

Bus Cap is raising RM24.69 mil from its public issue. For a Bursa listing, that is not a massive fund-raising exercise.

More importantly, the proceeds are not being raised to repair the balance sheet. They are being raised to expand production capacity, strengthen the corporate brand, increase market awareness and improve access to capital.

This distinction matters.

When an IPO is priced modestly with the proceeds directed into capacity expansion, the market tends to focus on whether the company can convert the capital into future earnings. For Bus Cap, that will be the real re-rating trigger.

Why forward valuation is more interesting

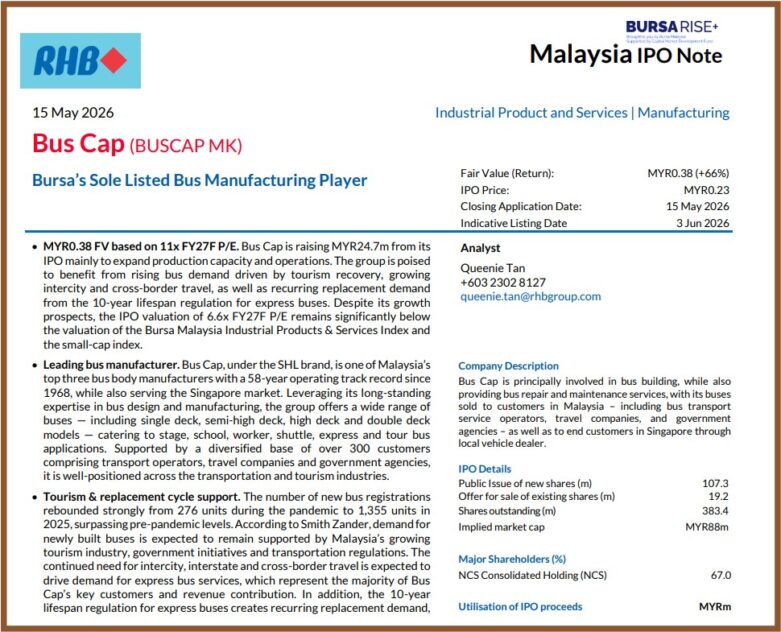

The Edge article further highlights Bus Cap’s conservative IPO valuation. RHB Research adds another layer to the story.

In its IPO note, RHB assigned Bus Cap a fair value of 38 sen/share which represents about 66% upside from the IPO price of 23 sen.

The research house valued Bus Cap at 11 times FY2027F earnings, broadly in line with the Bursa Malaysia Small Cap Index’s three-year average forward PE.

At the IPO price, RHB estimates Bus Cap is trading at 7.6 times its FY2026F earnings, 6.6 times FY2027F earnings and just 5.5 times FY2028F earnings.

This is where the proposition becomes more interesting for investors.

If Bus Cap can deliver the earnings growth projected by RHB, the current IPO valuation starts to look increasingly undemanding.

RHB forecasts revenue to rise from RM88.1 mil in FY2025 to RM106.4 mil in FY2026, RM120.6 mil in FY2027 and RM142.9 mil in FY2028.

Net profit is projected to grow from RM9.7 mil in FY2025 to RM11.7 mil in FY2026, RM13.3 mil in FY2027 and RM15.9 mil in FY2028.

This implies a three-year earnings compound annual growth rate (CAGR) of about 18%.

In short, the re-rating argument is simple: Bus Cap does not need to become a high-multiple stock overnight. If earnings continue growing and the market eventually values it closer to a normal small-cap multiple, there may be meaningful upside.

Capacity expansion the main catalyst?

Bus Cap’s current annual production capacity stands at 168 buses. The company plans to build a new factory and install a semi-automated fabrication line which is expected to increase annual capacity by about 15% to 194 buses.

The new factory will be located next to its existing Silibin premises in Ipoh. It will include a production plant, storage areas, a three-storey office building and a dedicated showroom.

The semi-automated line is not just about producing more buses. It is also intended to shorten cycle time, improve consistency and reduce reliance on certain manual processes.

For a manufacturing business, this can be important for margins, delivery timing and customer satisfaction.

The Edge article also noted that Bus Cap management sees the next one to two years of on-going orders as already secured with the key focus being execution – improving efficiency, shortening cycle time and increasing output.

That is why the IPO is more than just a listing event. It is a production-scaling story.

‘Demand is not just tourism’

Some investors may assume Bus Cap is mainly a tourism recovery play. That is only part of the story.

Bus Cap builds buses for express operators, tour companies, worker transport, shuttle services, stage buses and other commercial mobility needs.

Demand is supported by several structural drivers, including fleet replacement, public transport needs, intercity and cross-border travel, worker mobility and tourism.

According to RHB, Malaysia’s new bus registrations rebounded to 1,355 units in 2025 from 276 units during the pandemic, surpassing pre-pandemic levels. The research house also pointed to the 10-year lifespan regulation for express buses as a recurring replacement driver.

This means Bus Cap’s demand is not purely discretionary. Buses age. Operators need to replace fleets. Express bus operators need to maintain comfort and service standards. Students, workers and travellers still need transport.

Bus Cap ED Ng also noted in The Edge that unless an extreme event like a pandemic happens, demand for buses remains relevant because people still need to travel, students still need transport and tourism continues.

This gives the business a more defensive angle than a typical consumer-driven stock.

Customer stickiness, bottom line

Another point that stands out is customer diversification.

The number of customers served increased from 13 in FY2022 to 64 in FY2025 while Bus Cap’s cumulative customer base now exceeds 300.

The largest customer’s revenue contribution fell from 25.3% in FY2022 to 9.6% in FY2025 while the top five customers’ contribution dropped from 67.4% to 28.9%.

This matters because it shows that Bus Cap has been growing while reducing customer concentration risk.

In a niche manufacturing industry, customer trust is not built overnight. Buyers are typically concerned about quality, delivery track record, after-sales support and re-sale value. This makes it difficult for new entrants to compete purely on price.

Bus Cap’s IPO is a low-key entry into Bursa Malaysia but the re-rating set-up is worth watching.

The company has a 58-year track record, rising earnings, improving customer diversification, a supportive demand backdrop and a clear expansion plan.

At 23 sen/share, the stock is priced at about 8.98 times FY2025 earnings and based on RHB’s forecasts, only 6.6 times FY2027F earnings.

RHB’s fair value of 38 sen suggests that the market may eventually reward Bus Cap if it executes well.

For now, Bus Cap’s appeal is not hype. It is the possibility that a conservatively priced IPO, backed by real earnings and capacity expansion, may have room to rerate once the company starts delivering as a listed entity. – June 2, 2026