ACCORDING to the Construction Industry Development Board (CIDB), a total of RM126.7 bil worth of main contractor contracts were awarded year-to-date (YTD) as of end-August 2025, with government projects accounting for 26% and private projects making up 74%. Although this represents just 55% of 2024 total of RM230.4 bil, it is broadly in line with RM127.6 bil recorded in the first eight months of 2024.

“We maintain our annual contract award forecast of RM180 bil for 2024–2026. We believe more awards are on track, underpinned by ongoing public projects and robust private sector activity, particularly in data centres,” said Kenanga.

The upcoming Sabah State Election should also accelerate contract flows in the state. Kenanga remains positive on the construction sector’s up-cycle into quarter four calendar year 2025 (4QCY25), supported by both public infrastructure and private developments.

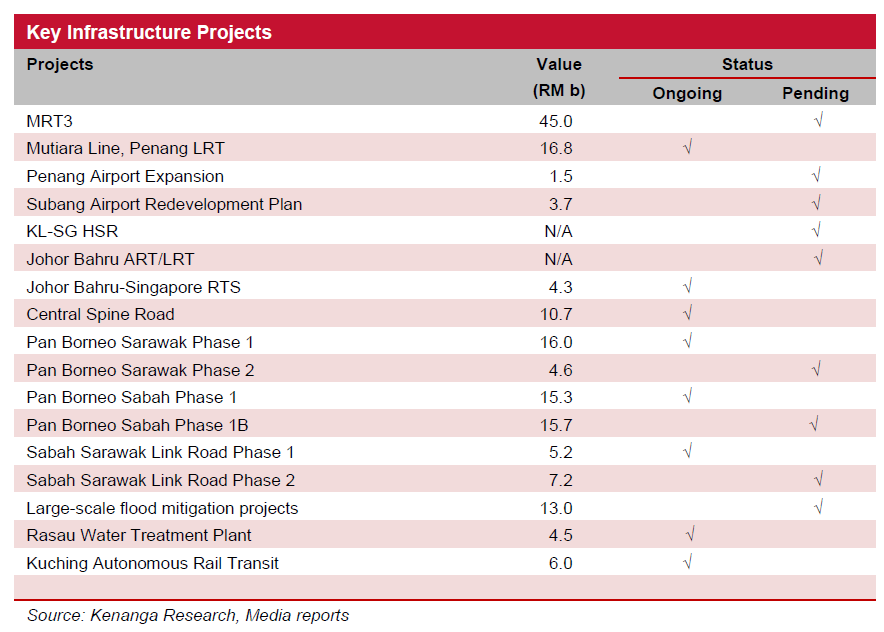

While the timeline on the MRT3, which has received final approval from the Transport Ministry, remains uncertain, several key projects are progressing, including the Penang LRT Mutiara Line Packages 2 & 3, Penang Airport expansion, Phase 2 of the Pan Borneo Highway, Sabah-Sarawak Link Road, Subang Airport redevelopment, and the Johor LRT/ART.

The KL–Singapore High Speed Rail remains a medium-term catalyst. Meanwhile, the Upper Padas Water Dam in Sabah and the EPCC contract for the Kerian Water project in Perak are still pending finalisation, though GAMUDA has already secured both water concessions.

In the first half of calendar year 2025 (1HCY25), at least two US tech giants, Microsoft and Pearl Computing acquired land in Malaysia for data centre expansion.

According to TENAGA, seven data centre projects (733MW) signed Energy Supply Agreements (ESAs) YTD to mid-Aug 2025, bringing the cumulative total to 47 projects (6,700MW), of which 24 projects (3,500MW) have been completed.

We expect the data centre boom to persist for at least the next two years and maintain our assumption of 700MW new capacity annually, equivalent to approximately RM21 bil in construction contract value annually.

The construction sector has outperformed this year, largely driven by the data centre boom, with the KLCON Index up 8% YTD vs the FBMKLCI’s -3%.

Kenanga maintains overweight for the sector. Despite slower-than-expected roll-outs of public projects, Kenanga remains bullish on the construction sector given persistent demand from data centres, fuelled by sustained capex from global tech firms.—Oct 8, 2025

Main image: PwC