MALAYSIA’S construction sector is poised for strong growth in 2026, building on a 16.6% surge in early 2025.

The industry is expected to expand at an average annual rate of 4% from 2026 to 2029, driven by high-value investments in hyperscale data centres, water infrastructure, and transport projects, alongside rising residential demand.

However, cost pressures have begun to filter through the system, driven mainly by higher diesel prices, which feed into logistics, transportation and material production.

Retail diesel prices in Peninsular Malaysia have risen sharply from around RM2.15/litre in early February 2026 to RM5.90–6.70/litre in April, and this is already reflected in building material prices, with cement and ready-mix concrete up 9.1% and 7.9% year-on-year (YoY) in Mar 2026, respectively.

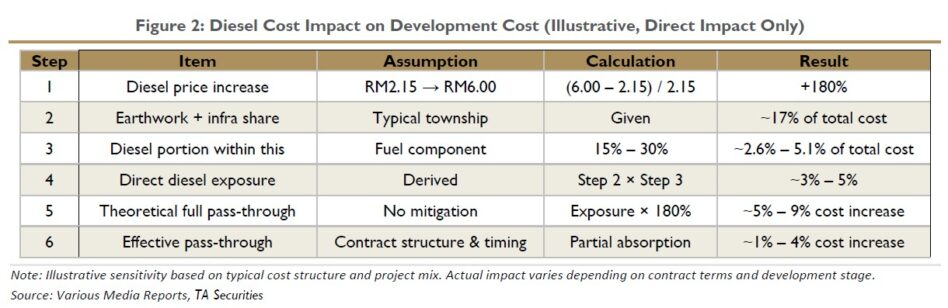

At the project level, the impact remains contained. As per the sensitivity analysis in our construction sector update report Headwinds emerging, but fundamentals hold dated 13 April, a 10% increase in diesel and material costs typically translates into a 1–2% increase in construction cost.

“Our estimates suggest that direct diesel exposure at the project level is around 3–5%, implying a theoretical 5–9% increase in cost under full pass-through,” said TA Securities.

In practice, however, the effective impact is lower at around 1–4% after factoring in contract structures, project timing and partial cost absorption.

Beyond direct diesel exposure, the more relevant risk lies in the spillover into the broader cost base. Higher fuel prices feed into transportation, logistics and material production, and this is already reflected in the increase in cement and ready-mix concrete prices.

While this effect is harder to quantify, it typically comes through progressively rather than all at once.

In practice, this does not translate into an immediate margin shock, as developers are able to adjust across the development cycle, with cost increases gradually reflected in pricing for new launches and subsequent phases.

There are no signs of changes to launch plans or sales targets, and pipelines remain intact.

Ongoing projects are largely protected by fixed-price contracts, while for new projects, the adjustment is mainly around timing, with some developers pacing tender calls to avoid locking in elevated costs.

Diesel usage is also concentrated in the early stages of development, particularly during site clearing and infrastructure works, with more limited exposure during the main construction phase. Despite concerns around rising costs, the sector has held up well.

The KLPRP Index has outperformed the FBMKLCI on a year-to-date basis, reflecting continued investor interest in the sector’s earnings visibility and structural growth drivers. At the same time, valuations remain undemanding.

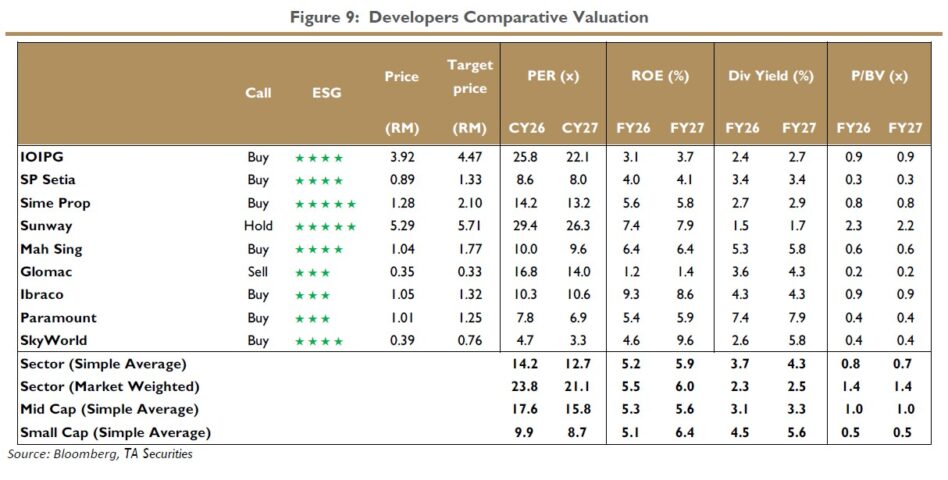

“Developers are trading around long-term average P/B levels, which we view as not fully reflecting the sector’s strengthening earnings outlook, supported by industrial land demand, data centre developments and steady project rollouts,” said TA.

TA maintains their Overweight stance on the sector. Earnings visibility remains supported, with unbilled sales across most developers generally above 1x of annual revenue.

Cost pressures are expected to be manageable, with increases gradually absorbed and recovered over time through pricing adjustments across successive launches and project phases.

“We maintain our earnings forecasts and target prices for developers under our coverage at this stage. The exception is Sunway,” said TA.

TA sees better resilience among developers with stronger balance sheets, good earnings visibility and exposure to industrial and data centre developments.

Their top pick is SimeProp, backed by its strong leadership in industrial development, robust financial performance, and expanding recurring income base.

Its hyperscale data centre projects, backed by approximately RM7.6 bil in contracted leases over 20 years, are expected to lift recurring income contribution to around 30% by 2028.

This strengthens earnings visibility and positions SimeProp as both a tactical and structural play within the sector. —Apr 17, 2026

Main image: CIDB