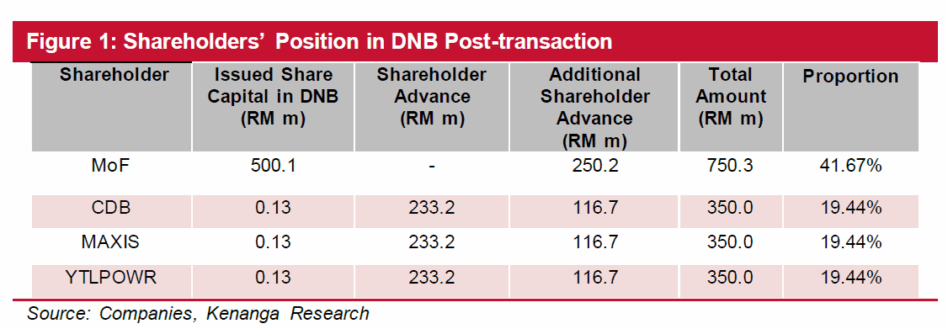

AT Digital National Berhad (DNB)’s request, each mobile network operator (MNO) shareholder, namely CDB, MAXIS, and YTLPOWR, has provided an additional shareholder advance of RM116.7 mil in cash.

Including earlier advances of RM233.2 mil, each MNO’s cumulative investment now totals RM350 mil, while each still retaining their 19.44% stake in DNB.

No further cash contribution is required from the Ministry of Finance (MoF), which holds a 41.7% stake in DNB, as its portion will be deemed to have been made out from the existing MoF loan of RM450 mil.

Accordingly, the outstanding loan balance owed to MoF is reduced to RM199.8 mil.

The shareholder advances, amounting to RM350 mil each, are intended to support DNB’s 5G operations, strengthen its financial position, and cover working capital requirements.

From the standpoint of MNOs, we understand that the risk-rewards are tied in with the following, including:

(i) DNB’s ability to generate sustainable revenues despite the option for access seekers to migrate to the upcoming second 5G network.

(ii) the extent to which DNB may require further funding to support 5G rollout and to optimize operations.

Nevertheless, to mitigate funding risk, a shareholder steering committee has been established within DNB, with a regular reporting obligation to ensure prudent management of funds.

We are neutral on this development, as the modest additional advances have negligible impact on CDB and MAXIS’ balance sheets. Assuming full funding via internal cash, the effect on leverage is minimal.

Furthermore, should the MNOs eventually exit DNB, their cumulative shareholder advances can be offset against future 5G access agreement fees payable to DNB.

To a certain extent, this mitigates the risk of financial loss for exiting shareholders.

Recall that in Feb 2025, DNB embarked on a corporate restructuring exercise involving a comprehensive revamp of its business plan, funding strategy, and operational framework.

As part of this initiative, DNB is engaging closely with shareholders and external consultants to strengthen its long-term sustainability.

We believe this fresh injection provides DNB with a near-term liquidity boost and could ease its interest burden on the outstanding MoF loan.

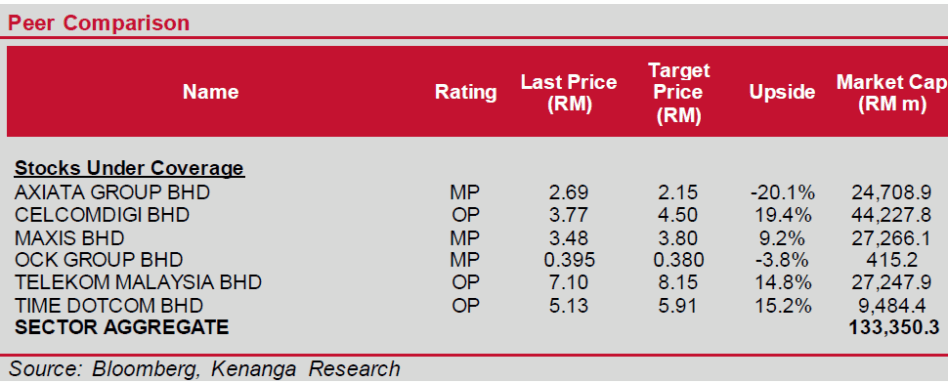

We retain our NEUTRAL view on the telco sector as we await greater clarity on the execution of the 5G dual network policy.

The eventual alignment of MNOs to either NW2 or DNB’s existing network will be a key determinant of the sector’s earnings trajectory, capex commitments, and dividend-paying capabilities.

In the meanwhile, we prefer fixed-line operators, which are less exposed to near-term policy risks. —Aug 18, 2025

Main image: ipleaders