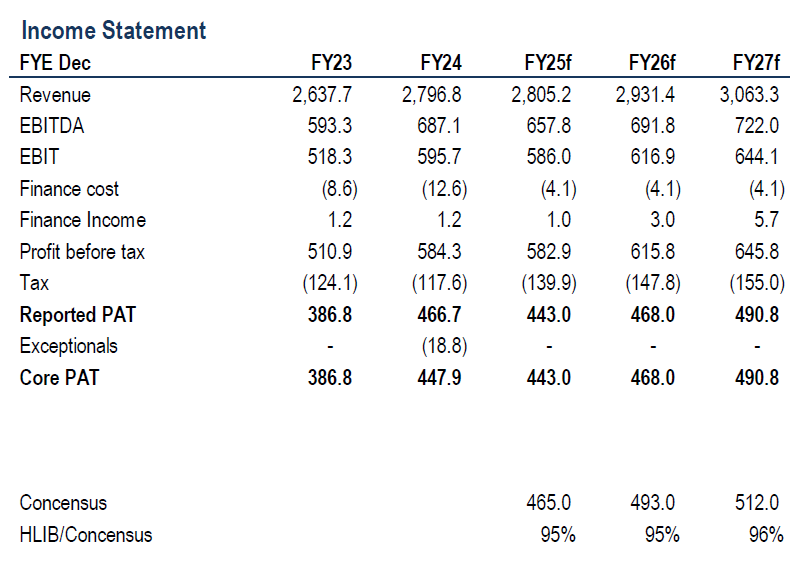

HEINEKEN’s quarter two 2025 profit after tax and minority interest came in at RM83.1 mil (-9.0% year-o-year), bringing the first half of 2025 core earnings to RM206.0 mil (-3.7% year-on-year).

The results fell short of both our and consensus expectations, accounting for only 44% of the respective full-year forecasts.

“The earnings miss was primarily attributed to weaker-than-expected margin performance in 2Q25, driven by higher costs associated with ongoing digital infrastructure investments,” said Hong Leong Investment Bank.

The decrease in sales was generally in line with Carlsberg’s 25% decline in its Malaysia operations.

Notably, higher expenses were recorded this quarter, which led to a 0.9 points erosion in earnings before interest and tax margin, as the group continued to invest in commercial initiatives and its digital infrastructure.

Following Heineken’s announcement of a 2%-8% beer price increase, we expect some frontloading of volumes in the upcoming quarter, in line with previous patterns.

While the financial impact of past price increases on brewers has generally been neutral rather than negative, supported by relatively inelastic demand, Heineken’s ongoing spending in digital infrastructure could weigh on Heineken’s near-term profitability.

Although management has not explicitly confirmed whether these costs will continue into the second half of 2025, it has characterised the initiative as an ongoing process to improve operational efficiency, suggesting that related expenses may persist beyond the current period.

Separately, regulatory headwinds remain a key risk, with the government recently extending the pro-health tax to brewers and expressing support for a potential increase in cigarette taxes.

We continue to like Heineken for its strong brand equity and leadership position in the Malaysian market. —Aug 18, 2025

Main image: Wikipedia