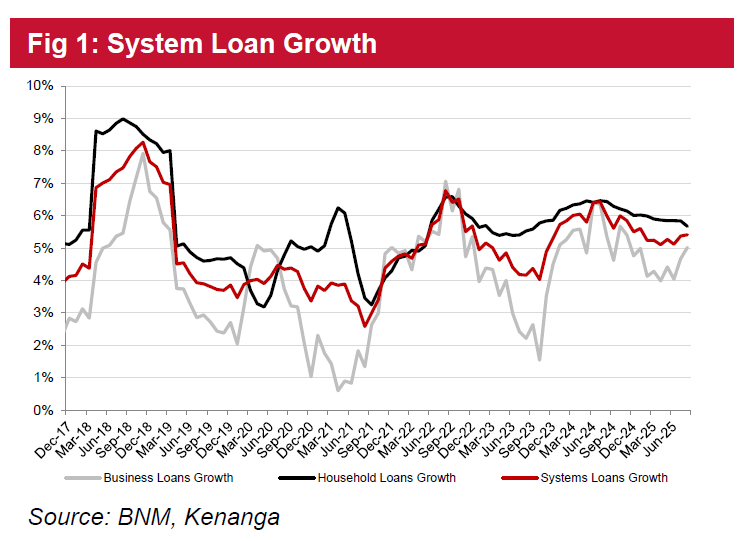

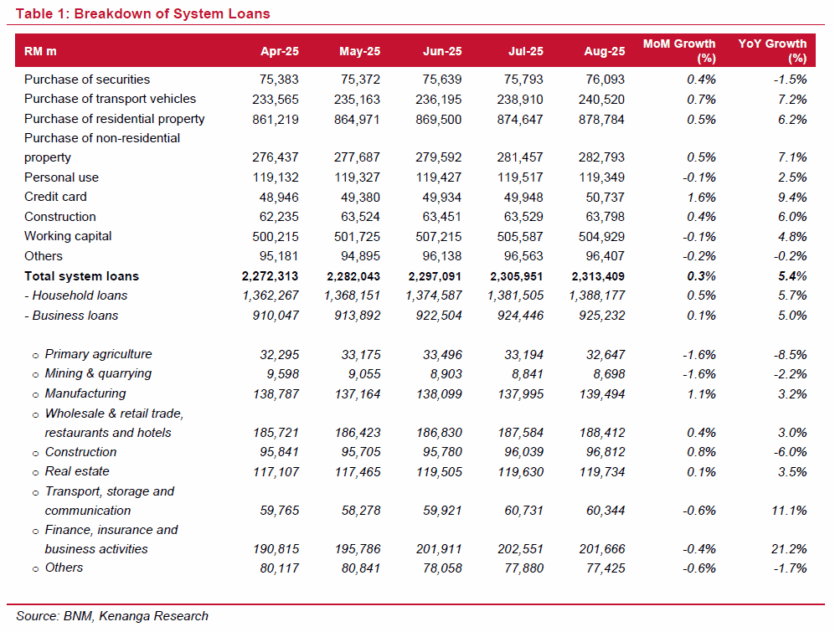

AUG 2025 system loans grew by 5.4%, within Kenanga Research’s 5.5% target for calendar year 2025 (CY25).

Kenanga anticipates an uptick in the second half of calendar year 2025 (2HCY25) on backloaded household applications (mortgage, hire purchase) and business loans (working capital).

On a year-on-year (YoY) basis, household loans grew by 5.7% with sustained demand for transport vehicles and residential properties.

Meanwhile, business loans increased by 5.0% on the back of continued working capital needs led by the service sectors.

On a month-on-month (MoM) basis, household loans saw higher momentum than business loans thanks to stronger demand for hire purchases.

System loan applications only increased by 2% YoY and were flattish MoM. The muted reading could be attributed to the surge of applications in July 2025 post-25 basis points overnight policy rate (OPR) cut.

The higher base effect was mainly led by the household segment, which reported a 4% decline MoM across all application purposes, even on residential property and transport vehicles.

“Still, we continue to see applications for working capital loans to be unhindered, growing by 6% MoM against the overall business loan application growth of 5%,” said Kenanga.

System loan approval rate came in at 50.6% which we opine could increase in the coming months from the gradual processing to the application backlog.

Aug 2025 deposits grew by 3.8% with stable current account savings account (CASA) of 28.9%. CASA products are likely to remain out of favour from depositors with interest rates continuing to be unattractive, where we believe alternative storage of cash may be more sought after (trading accounts, unit trusts).

Industry LDR continued to stretch further to 89.4% following the stronger support in loans growth. Against our expectations that there would be no more OPR movements during the year, it is likely that deposits growth would remain muted as deposit rates may only grow less attractive.

Moving into the quarter four of calendar year 2025 (4QCY25) season, We believe the sector will remain resilient despite economic headwinds that could moderate loan growth, supported by their better expectations for their investment portfolios to sustain earnings.

We do not anticipate asset quality risks, on the back of the sector already being fairly well-provisioned and asset quality risks being limited.

In spite of the added precaution by the sector against US tariffs, return on equity expectations remain stable and even with slight increases, which should anchor expectations on the sector in the near-term. —Oct 1, 2025

Main image: The Economic Times