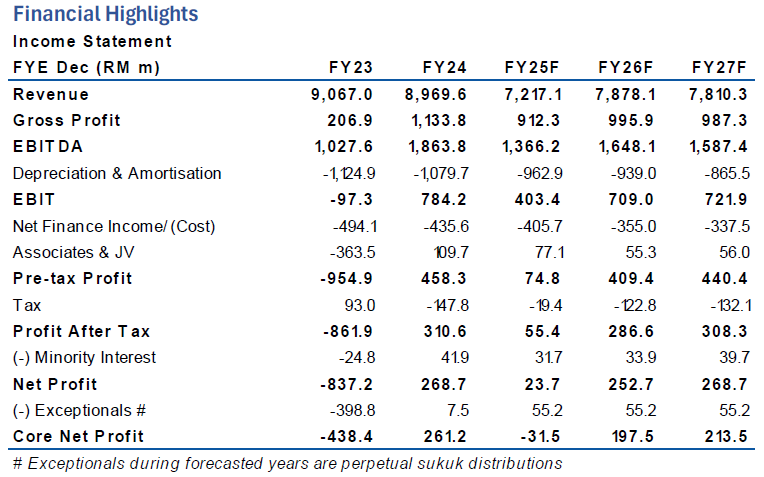

MALAKOF slipped into a core net loss (CNL) of RM38.6 MIL in QUARTER THREE FINANCIAL YEAR 2025 (3QFY25), bringing nine months of financial year 2025 (9MFY25) core net profit (CNP) to RM40.1 mil.

The underperformance was driven mainly by capacity income loss at TBE following the steam turbine crossover pipe leakage and a substantial drop in associate/JV contributions after the decommissioning of the Shuaibah Water & Electricity Company (SWEC) plant.

3QFY25 posted a CNL of RM38.6 mil versus a CNP of RM86.9 mil in 3QFY24.

“The decline was driven primarily by RM30 mil in lost capacity income arising from TBE’s unscheduled outage and a 61.4% drop in associate/JV contributions following the decommissioning of SWEC’s plant in May 2025,” said APEX Securities.

This was recorded despite a narrower negative fuel margin. TBE was offline from 8 Sep to 16 Oct due to steam turbine crossover pipe leakage, during which its unplanned outage rate (UOR) exceeded the 6% threshold on 16 Sep and subsequently rose to 12%, breaching both PPA thresholds.

“Meanwhile, Shuaibah’s profit contribution fell 79%, consistent with its reduced operating profile post-decommissioning,” said APEX.

MALAKOF swung from a CNP of RM26.7 mil in 2QFY25 to a CNL of RM38.6 mil in 3QFY25. The sequential deterioration resulted from the capacity income shortfall at TBE, the weaker contribution from Shuaibah, and the recognition of RM27.8m in perpetual sukuk distributions that were not present in the preceding quarter. This was partially offset by a smaller negative fuel margin.

9MFY25 core net profit contracted 81.7%, pressured by the 3Q outage at TBE and the sharp reduction in Shuaibah’s profit contribution. The results were further weighed down by lower earnings from Prai Power Plant following the expiry of its extended PPA in August 2025 without renewal.

Incremental contribution from the 49% stake in E-Idaman, acquired in February 2025, only partially mitigated the shortfall.

“We downgrade MALAKOF to SELL (from HOLD). No ESG premium or discount applied given its three-star rating,” said APEX.

While MALAKOF remains well-positioned to secure future gas-plant PPAs due to its scale, APEX expects near- to medium-term earnings to remain under pressure, with meaningful improvement only after 2028 once new assets begin contributing. —Nov 28, 2025

Main image: The Malaysian Reserve