MALAYSIA is one of the world’s top six semiconductor exporters, accounting for roughly 7% of global exports and about 13% of the global assembly, testing, and packaging market.

Any substantial tariff on semiconductors would inevitably weigh on Malaysia, as the industry is deeply integrated into global supply chains.

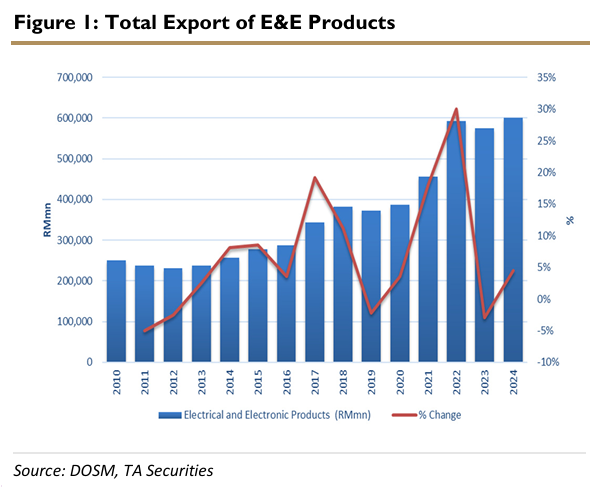

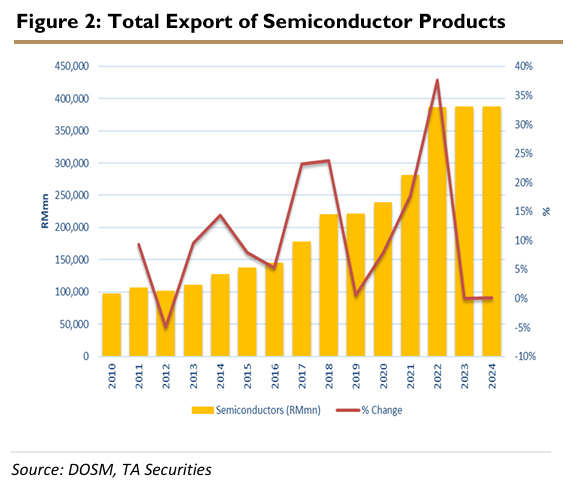

In 2024, the country exported approximately RM120 bil worth of electrical and electronic (E&E) products to the US, representing around 20% of total E&E exports.

Notably, semiconductors made up RM60.6 bil of that figure, highlighting the sector’s strategic role in Malaysia–US trade.

Therefore, a steep tariff could undermine Malaysia’s export performance, as higher tariffs would drive up production costs, part of which may be passed on to customers, ultimately weighing on demand.

Against the backdrop of looming tariffs, we believe the impact will likely be less severe than initially anticipated, as roughly 65% of Malaysia’s semiconductor exports to the US come from American firms operating in Malaysia, which could be eligible for exemptions.

“Generally, we believe there is a high likelihood that most major US-based multinational companies have the financial strength and capabilities to invest in the US to mitigate the impact of these semiconductor tariffs,” said TA Securities.

On top of that, we expect more conditional exemptions to be introduced over time, given the complexity and interdependence of the global semiconductor supply chain.

Overall, we believe it would be extremely difficult for the US to fully repatriate the semiconductor value chain in the near term, as building a self-sufficient ecosystem would likely take decades.

Although the semiconductor companies under our coverage (INARI, UNISEM, and MPI) derive a sizeable portion of revenue from US customers, their direct export exposure to the US remains limited.

This is because most of their products are supplied to intermediate customers, who subsequently integrate the components into modules or finished products before exporting to another locations.

Among the three, INARI should be the least affected, as it does not ship any components directly to the US. UNISEM has guided that approximately 90% of its products are destined for the Asian market, while MPI’s direct exposure to the US is estimated at below 10% of total revenue.

Nonetheless, despite their minimal direct exposure, these companies could still face indirect headwinds should overall end-demand soften due to the imposition of hefty tariffs.

In July 2025, the global semiconductor sector sustained its upward trajectory, with sales registering another notable increase.

According to the Semiconductor Industry Association, global semiconductor sales rose to USD62.1 bil in July 2025, marking the 21st consecutive month of YoY growth, underpinned by sustained demand for AI and high-performance computing applications.

The YoY growth was supported by all regions except Japan (-6.3% YoY). The Asia Pacific/All Other led the growth (+35.6% YoY), followed by Americas (+29.3% YoY), China (+10.4% YoY), and Europe (+5.7% YoY).

While global semiconductor sales are projected to continue growing, we maintain a cautious outlook given the lingering uncertainties surrounding US trade policy.

On the domestic front, we expect the Malaysian government to remain committed to the National Semiconductor Strategy, which aims to strengthen the country’s position in the global semiconductor value chain. Overall, we reiterate our neutral stance on the semiconductor sector. —Sept 12, 2025

Main image: Reuters