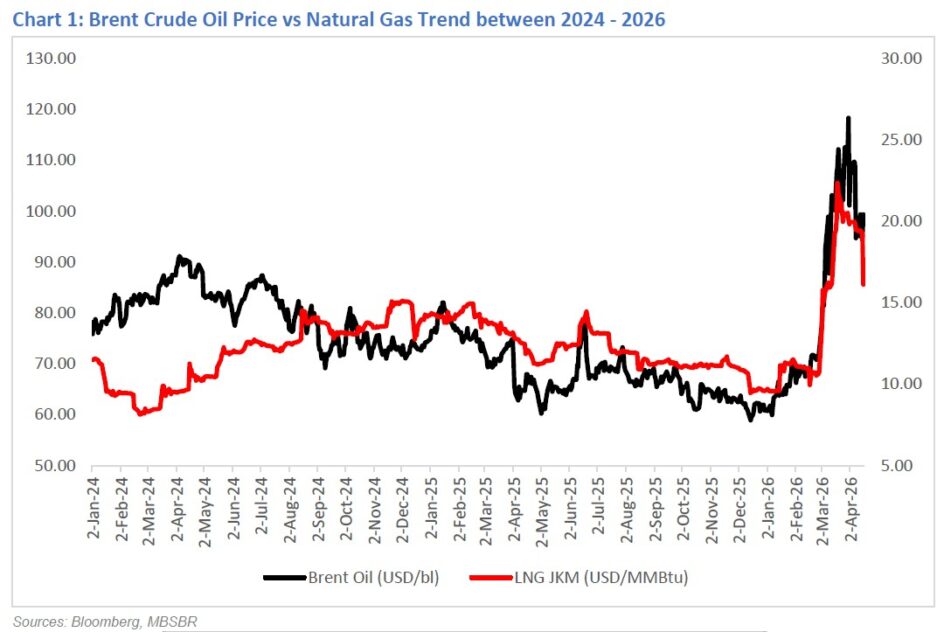

THE INTERNATIONAL Energy Agency has significantly downgraded its 2026 oil demand forecast, shifting from expected growth of 730,000 barrels per day to a contraction of 80,000 bpd.

This revision reflects what it describes as an unprecedented supply disruption, which has pushed crude prices above USD110 per barrel and introduced a stronger supply-driven risk premium into the market.

Sustained high oil prices and ongoing supply tightness are now feeding through to downstream industries.

The petrochemical sector, in particular, is slowing noticeably as affordability pressures intensify and access to feedstock becomes more constrained.

Across Asia, producers are scaling back operations due to limited availability of key inputs such as naphtha and LPG, resulting in a shift away from previous oversupply conditions towards a tighter, scarcity-driven market.

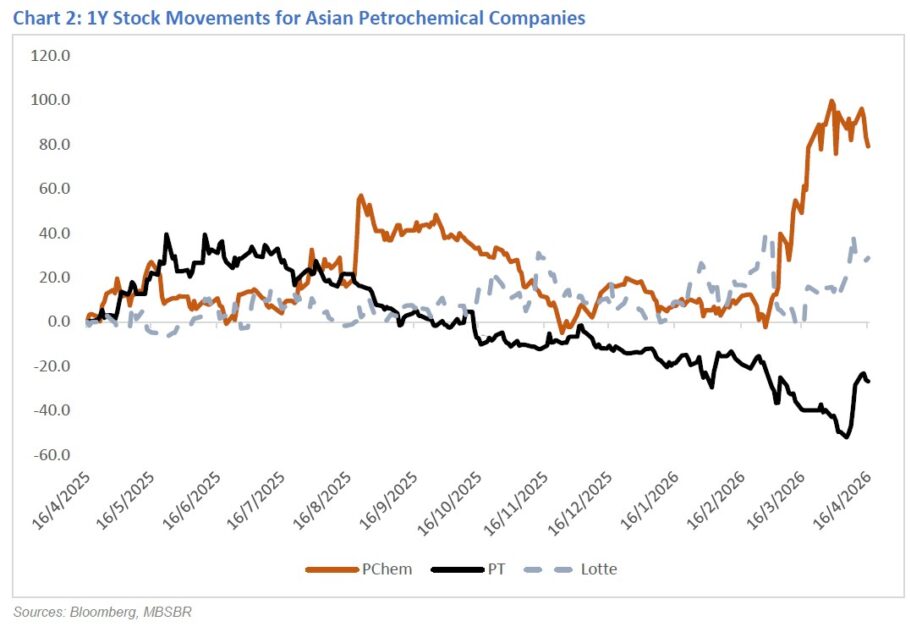

The situation has been further complicated by Force Majeure declarations from major regional players, including PT Chandra Asri Pacific and Lotte Chemical.

These developments underscore the fragility of the “just-in-time” supply model, particularly for import-reliant markets like South Korea, Singapore and Indonesia, which remain especially exposed to supply disruptions.

In contrast, Petronas Chemicals Group is relatively well shielded due to its access to domestic natural resources. Its operations are largely anchored on natural gas, providing a more stable and secure feedstock base.

This advantage has translated into stronger share price performance during the current turmoil, as investors favour companies with more reliable input access.

Performance comparisons highlight this divergence. Petronas Chemicals posted a robust 79.2% year-on-year gain, outpacing Lotte Chemical, which rose 28.8% over the same period.

Meanwhile, PT Chandra Asri Pacific saw its share price fall by 26.8%, reflecting its higher vulnerability to feedstock shortages and supply chain disruptions.

In the current environment, access to feedstock has become a critical differentiator. Companies with domestic resource advantages are demonstrating greater resilience compared to those dependent on imports.

Against this backdrop, Petronas Chemicals Group stands out as a relative outperformer, and we maintain our BUY recommendation with a target price of RM6.60. —Apr 17, 2026

Main image: Bloomberg