THE management of Public Bank Bhd (PBK) maintains that it will be relying on Non-Interest Income (NOII) (more specifically, improvements in bancassurance and unit trust performance) to compensate for the reduced Net Interest Income (NII).

The Group will not be using overlay releases to achieve the return on equity (ROE) target if earnings are lacking. “We think this is overly optimistic and opine that the Group will not be achieving its 13% ROE target,” said MBSB Research.

From a loan yield perspective, residential mortgages and SME loan segments remain highly competitive. Regardless, management still feels relatively optimistic about its COF outlook.

Alternative funding methods (RM1.6 bil of senior debt was recently issued) seem promising. The Group notes that its peers have been pricing retail deposit rates downwards, implying that the industry as a whole can reduce reliance on pricier institutional deposits.

While PBK has been losing market share over the last couple of years, management highlights that its current cost per deposit account is far lower than that of its peers.

If it means avoiding high-cost current account savings account campaigns, the group is willing to trade off market share to preserve its margins.

On the subject of its financial year 2025 (FY25) deposit growth target of 4-5%, the Group feels that it is trailing this figure well in the first half of financial year 2025 (1HFY25) and does not feel overly pressured to deliver.

After last year’s disappointing loss due to asset quality issues, this year is seeing improving margins and some stabilisation on asset quality. From management’s perspective, the big question is the extent of recovery achievable.

Recall that management was given until FY26 to dispose of these shares, we feel, however, that management has the potential to prolong the deadline if market conditions remain lacklustre.

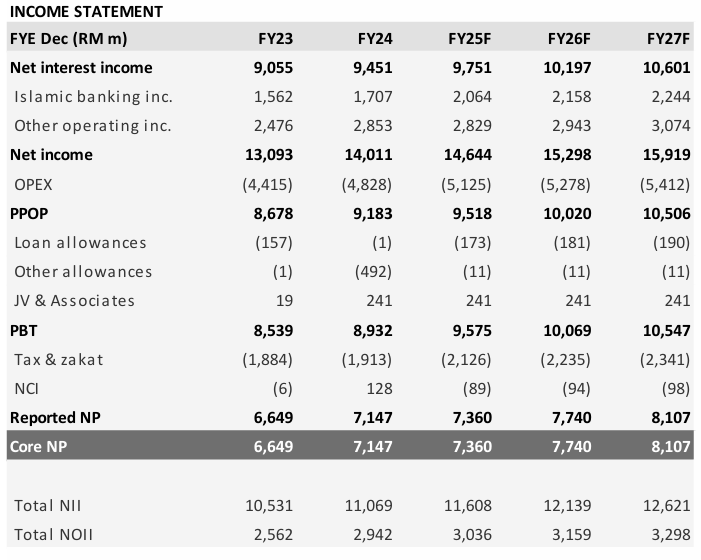

Forecasts unchanged. We make no changes to our earnings forecasts. Key downside risks identified are the lower-than-expected loan growth, weak NOII performance, steeper-than-expected NIM compression. MBSB maintains its buy call. —Aug 27, 2025

Main image: Reuters