THE ENERGY sector’s quarter four 2025 (4Q25) earnings met expectations.

Of the nine companies under RHB’s coverage that reported results, two booked numbers that came below estimates, two outperformed, and the rest were in line.

The results of the big-cap players (market cap above MYR2 bil), which make up 71% of RHB’s energy sector coverage, were within expectations.

TNB recorded a lower effective tax rate (ETR) during 4Q,which was in line with our, but ahead of Street assumptions.

YTLP also saw stronger contributions from its water segment, which mitigated the softer performance from its power generation business.

The former’s earnings fell 7% year-on-year (YoY) due to a higher-than-expected ETR and operating expenses, while the latter was impacted by disruptions at its coal plants.

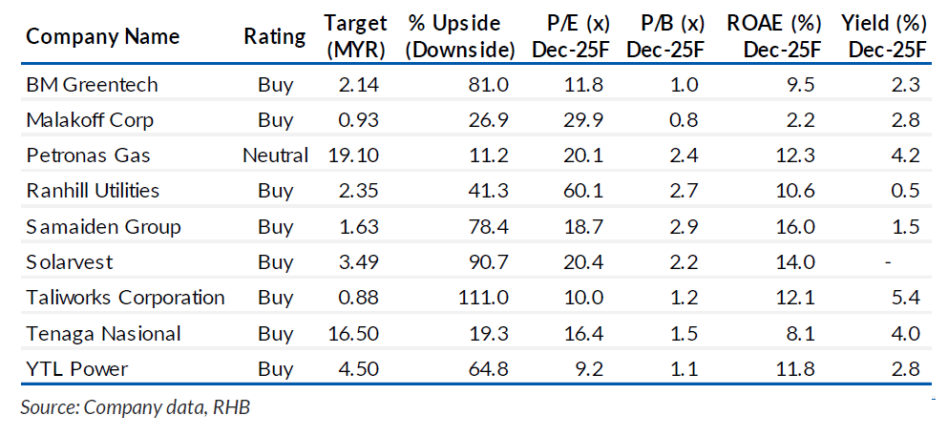

“Among the solar names under our coverage, Samaiden surprised on the upside due to the progressive recognition of several utility-scale projects,” said RHB.

Meanwhile, Solarvest’s earnings were in line, with its outstanding orderbook rising 16% QoQ to a record high of MYR1.5 bil.

In the water utility space, Ranhill Utilities (RAHH) pulled off an outperformance due to stronger-than-expected margins post tariff hike, while Taliworks Corp’s (TWK) earnings were in line.

“We like energy as a defensive sector, should the geopolitical tensions persist, resulting in a market risk-off mode,” said RHB.

This is because big-cap utility names have minimal exposure to non-domestic risks, while regulated frameworks provide stable earnings with 4-5% dividend yields.

“In addition, we see YTLP as a potential beneficiary of an increase in gas prices, resulting in higher spark spreads,” said RHB.

Meanwhile, the cost pass-through mechanism for TNB’s and PTG’s regulated business ensures that cost fluctuations will have a neutral impact on their earnings.

RHB leans towards TNB, YTLP and PTG in a risk-off environment, further maintaining their Overweight call on the sector.

TNB remains their Top Pick, as it is the prime beneficiary of the National Energy Transition Roadmap, with the regulated framework providing a stable earnings base.

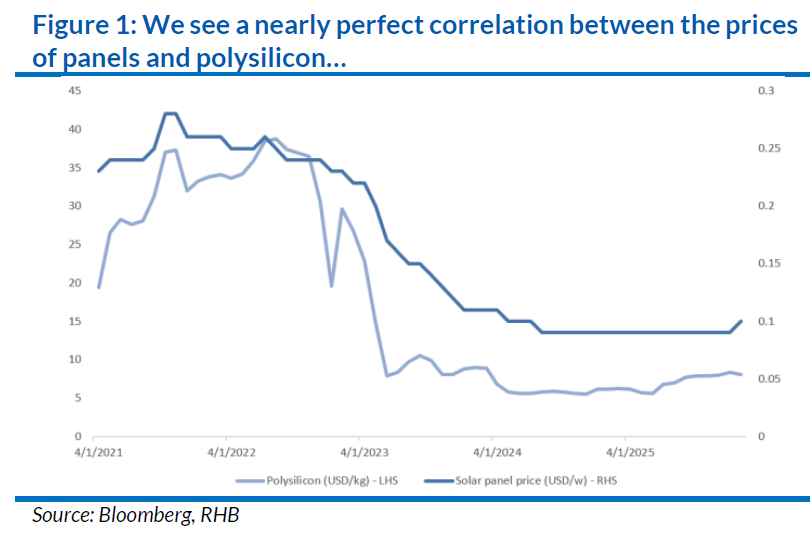

RHB encourages investors to accumulate Solarvest and Samaiden shares following the recent correction, as they expect to see a minimal impact from the removal of the export value-added tax rebate on the solar players. —Mar 10, 2026

Main image: Kenueone