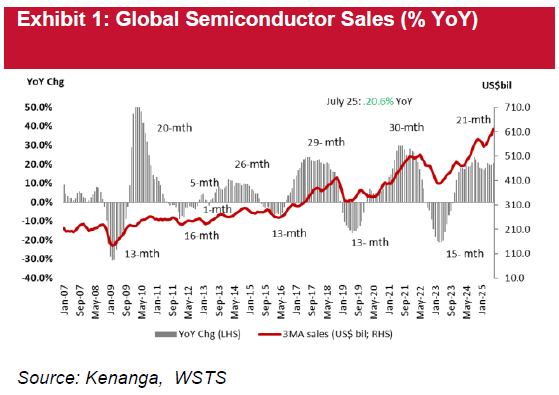

JULY global semiconductor sales have reclaimed the more than 20% year-on-year (YoY) growth threshold, signalling not only resilience but also sustainability of the current up-cycle.

Growth continued to be led by Logic and Memory on robust data-centre spending and early AI-edge adoption. Importantly, the clearer direction on global tariff policies has reduced trade uncertainty, reinforcing visibility into demand momentum.

With structural tailwinds from AI, HPC, 5G, and next-generation smartphones, the present 21-month rally is showing no sign of fading.

“We believe the current cycle could extend beyond 30 months, the historical longest upcycle period, marking a potential new peak for the industry,” said Kenanga Research.

Kenanga expects Budget 2026, scheduled for tabling on 10 October 2025, to deliver targeted support for Malaysia’s semiconductor ecosystem in line with the NSS, potentially via incentives, talent programmes and enablement for advanced packaging/design.

With more than RM63 bil of investments already secured since launch, the government has identified 13 NSS-flagged champions across the value chain—including Carsem, Inari, Pentamaster, ViTrox, KGB, Greatech and several IC design firms (Oppstar, SkyeChip, Infinecs, Experior) that are well placed to benefit from favourable policies, subsidies, and capacity-building measures.

We advise investors to focus on these names, where policy tailwinds and facilitation are most likely to be concentrated. Also, the global auto outlook is turning more constructive, with EV penetration and software-defined features driving incremental content growth.

China remains the largest market, Europe continued to benefit from decarbonisation-linked incentives, and US demand is stabilising ahead of tax credit expiries.

A firmer quarter four (4Q) is anticipated as subsidies resume and seasonal demand improves, further supporting the recovery. This backdrop should benefit the broader automotive semiconductor and LED ecosystem.

In Malaysia, MPI (auto test/OSAT exposure) and D&O (automotive LEDs) are well placed to ride the recovery, supporting improving utilisation, order visibility and medium-term earnings.

Our channel checks suggest recent tariff adjustments have had contained direct impact on Malaysian technology companies, as most players sit mid-to-downstream with low direct US exposure.

While quarter two of calendar year 2025 (2QCY25) saw temporary headwinds due to order push-outs and uncertainty as customers revisited supply strategies, finalised tariff treatment has brought much-needed clarity. Importantly, we gathered that orders are now resuming, with minimal cancellations and costs largely passed through to clients.

While we see reciprocity risk higher for some EMS exposures, customer pass-through remains the base case. We expect business operations to normalise in 3QCY25, improving earnings visibility across the sector. —Sept 30, 2025

Main image: PWC