MAH Sing Group Berhad experienced a sharp sell-down in 2025, with the share price retracing ~46% from its yearly high. The correction was driven largely by sentiment surrounding the Bridge Data Centre (BDC) collaboration and global AI-chip restrictions.

“In our view, this fear-driven de-rating has materially disconnected the share price from underlying fundamentals,” said TA Securities (TA).

At RM0.965, TA believes Mah Sing’s fundamentals are over-discounted, creating an attractive asymmetric risk-reward entry point.

“With downside risks largely priced in, our Top Pick conviction is anchored by intact core earnings visibility and structural exposure to Malaysia’s next growth phase, spanning infrastructure, digital economy and manufacturing-led industrialisation,” said TA.

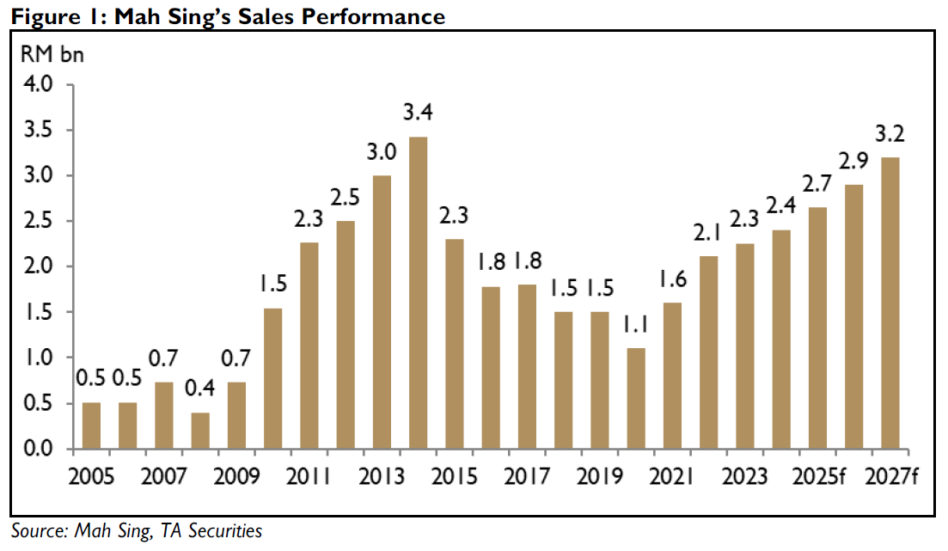

Mah Sing’s core operating fundamentals remain intact. Financial year 2025 (FY25) property sales are on track to meet the RM2.65 bil target, with the nine months of 2025 (9M25) achieving 72% of full-year sales.

Separately, unbilled sales of RM3.14 bil, an eight-year high, provide strong earnings visibility into 2026.

The balance sheet remains healthy, with net gearing at 0.25x and cash of RM1.17 bil, providing sufficient headroom to fund ongoing developments, pursue selective land acquisitions and sustain dividends amid a more volatile backdrop.

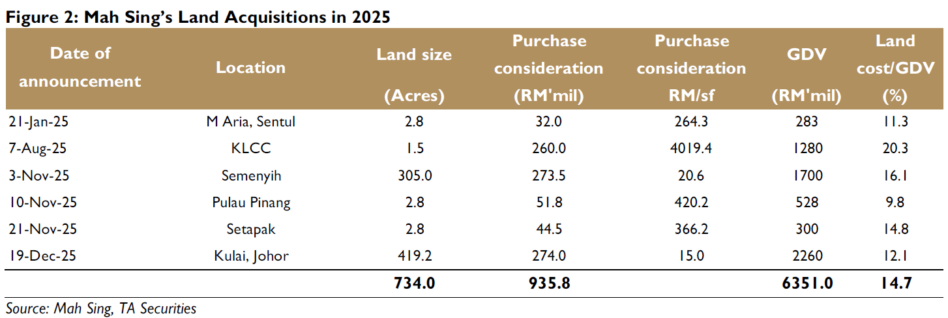

Notably, Mah Sing replenished RM6.4 bil of gross developmental value in 2025, making it one of the more active developers in land acquisition. This was achieved without significant balance-sheet strain and reinforcing the group’s ability to sustain launches and earnings momentum beyond 2026.

Mah Sing’s landbanking is increasingly aligned with major transit-oriented developments. Key examples include M Grand Minori near the Johor Bahru–Singapore RTS and M Cora near the upcoming Penang LRT.

As these projects reach key milestones, improved connectivity is expected to support buyer sentiment, pricing and inventory turnover, underpinning sustainable residential demand.

With prior DC collaboration agreements having lapsed, no material capital has been committed, while Mah Sing retains control over strategic land, power access and infrastructure readiness.

Management is evaluating outright land sales or selective BTL structures, depending on risk-return dynamics. While BTL is capital intensive, it would only be pursued with firm operator commitments.

Meanwhile, outright land sales to DC operators offer faster monetisation with lower execution risk. With the market currently assigning zero value to this segment, any DC monetisation represents incremental upside not reflected in current valuations, aligned with Malaysia’s longer-term digital economy ambitions. —Jan 2, 2025

Main image: Mah Sing