WITH the exception of earnings misses at CDB and OCK Group (OCK), and a slight beat for Maxis, most telcos reported in-line with quarter two (Q2) results.

Cost pressures continue to be well managed, with sector earnings before interest, tax, depreciation and amortisation (EBITDA) holding up despite the subdued revenue momentum.

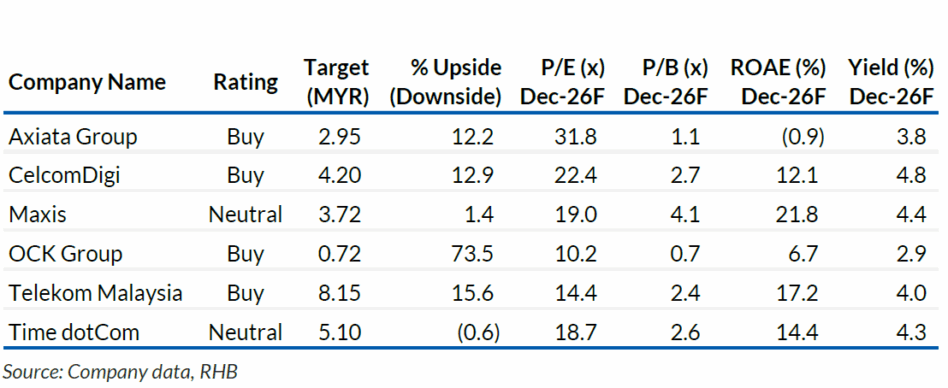

“We continue to like the fixed line players on structural catalysts and the more resilient earnings profile. Stay neutral,” said RHB.

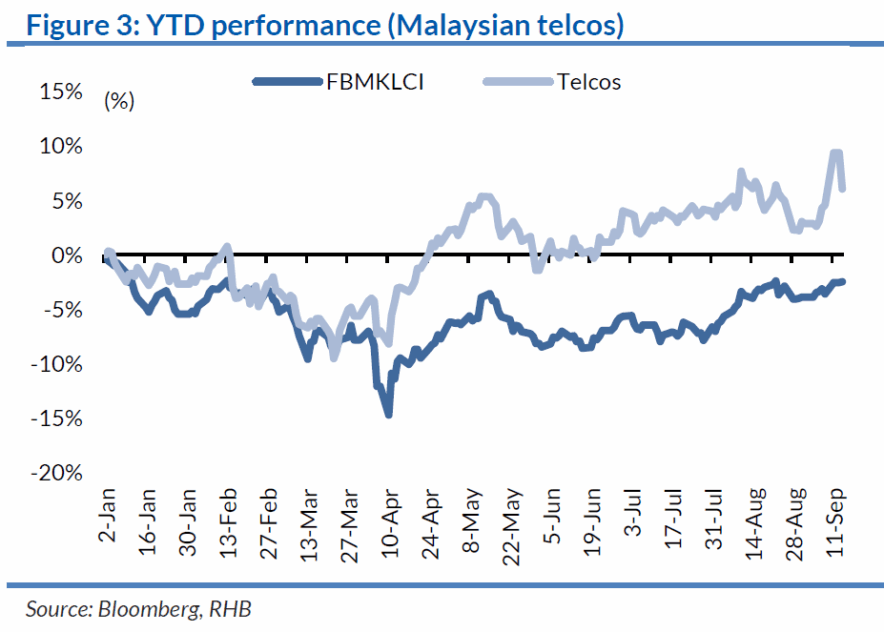

Relative to the ASEAN-4 peers, Malaysian telcos were ahead of Indonesian (+5.3%) and Thai (+1.5%) peers but trailed Singaporean companies (+18%).

Mobile service revenue was relatively steady quarter-on-quarter (QoQ) but fell 1.2% year-on-year (YoY) in 2Q25 as blended average revenue per user (ARPU) (Big-2 MNOs) slipped 1.5% from SIM consolidation and price competition.

That said, aggregate sector EBITDA (excluding Axiata) inched higher by 1% YoY in 2Q25 on tight cost controls.

Specifically, Maxis’ 2Q25 EBITDA grew 5% with its EBITDA share rising quarter to 44.1%. 5G access costs for MNOs were steady (MYR50-55 mil), despite higher 5G traffic with industry 5G subs up 45% quarter-on-quarter (QoQ).

On the expanded sales and services tax on tower rentals, MNOs highlighted ongoing discussions with the Government with a potential worst-case earnings impact of 1-5% on an annualised basis.

Industry fixed line revenue fell 3.3% YoY in 2Q25, led by the 4.7% drop in TM’s retail internet revenue, which slipped for the second quarter in a row as competition and promotional offers crimped ARPU with lower subs growth.

In contrast, Maxis’ home revenue, including wireless broadband service, held up on steady ARPU and subs-adds. TDC and CDB delivered stronger home fibre revenue (+3-9% QoQ) with fibre footprint expansion and up-selling of fibre bundles.

Most telcos have affirmed their financial year 2025 future (FY25F) revenue and EBIT/EBITDA guidance, with Maxis guiding for higher capital expenditure.

Post results, we lowered Axiata, CDB, Maxis and OCK’s FY25F-27F earnings but left our forecasts unchanged for the other telcos.

While Axiata’s earnings were marred by the stronger MYR, one-offs and impairments, we note financing charges fell 27% in 1H25 from the repayment of USD250 mil (MYR1.1 bil) holdco debt in 2Q25.

We expect additional interest savings into 2H25/FY26 as holdco debt is further reduced with the proceeds raised from the sale of edotco Myanmar in June.

Key risks to our forecast and calls are competition, weaker-than-expected earnings/margin, FX, and regulatory setbacks. —Sept 24, 2025

Main image: strategyandpwc.com